Global grain and oilseed prices remain high. Whilst a key driver is the war in Ukraine, there are also a number of other factors at play; there are concerns for crops in the US, EU, and India which are supporting new crop values.

EU Crop Conditions

Conditions in continental Europe have mirrored conditions in the UK. Many countries, including France, Germany, and Romania have experienced a lack of rain. For France and Germany, two key grain and rapeseed producers this situation does not look like changing before the end of May.

French agency FranceAgriMer has downgraded its view of winter cereal crop conditions. The EU crop monitoring report from the EU Joint Research Centre, published on 23rd May, further highlights the challenge of dry conditions but is still optimistic on yield impact. If conditions remain dry, a yield impact is to be expected, this will support the global grain price.

India

India has grown in importance to global grain markets in recent years. The third largest wheat producer in the world, after the EU and China, is forecast to export 8.2 million tonnes of wheat in 2021/22, rising to 8.5 million tonnes in 2022/23. However, dry conditions over the past couple of months has sharply reduced forecasts of output for the 2022 harvest. This has prompted the Indian government to ban exports of the grain. However, immediate concerns were softened, with sales to countries with irrevocable letter of credit to be honoured.

USA Crop Conditions

While US winter wheat crop conditions are unchanged on the month, they continue to be a concern. Drought conditions are observed in some of the key wheat producing states and also in parts of the High Plains (important for spring wheat). Maize plantings are also lagging behind the five-year average, as are spring wheat plantings. This is most notable in North Dakota, which produces more than 50% of the US spring wheat crop (6.9 million tonnes, 2017-2021 average). Crop conditions in the US will be watched closely over the coming weeksa and will be a key driver of grain prices.

USDA Supply and Demand Estimates

The USDA published its latest Supply and Demand estimates on 12th May. The report included the organisation’s first forecasts of the 2022/23 crop. Both the maize and wheat supply and demand balance are expected to tighten.

The stocks-to-use ratio for wheat is forecast to be the tightest since 2014/15 at 34.1%. However, China is also expected to accumulate more stocks in 2022/23. Excluding China from the analysis tightens global wheat stocks to the tightest point since 2007/08.

For maize, global stocks-to-use is seen falling slightly year-on-year. Conversely, global maize stocks-to-use, excluding China, is set to rise. This may add some downward pressure to maize prices, widening the gap to wheat. If the gap is favourable for consumers, this may also undermine wheat prices slightly.

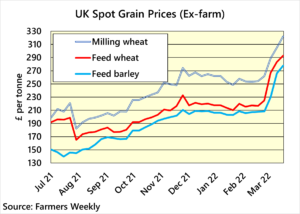

A week is a long time in politics, and given their intertwined nature at present, so too in grain markets. As the war in Ukraine enters into its second month, the impact on grain and oilseed markets has been considerable. This is not surprising when we consider the reliance the world has on both Ukraine and Russia for grain and oilseed supplies.

A week is a long time in politics, and given their intertwined nature at present, so too in grain markets. As the war in Ukraine enters into its second month, the impact on grain and oilseed markets has been considerable. This is not surprising when we consider the reliance the world has on both Ukraine and Russia for grain and oilseed supplies.