Looking out onto a very soggy Leicestershire, it seems that this November and December might have been as wet as the last. The difference is that, this year, most winter crops have been drilled already, and, on the whole, established better than last year too. Certainly, in this part of the East Midlands, if something has not been drilled by now, it has little chance now until the spring – a similar scenario to last year. There have, at least so far, been few frosts and cold icy mornings, perhaps the New Year will treat us to some.

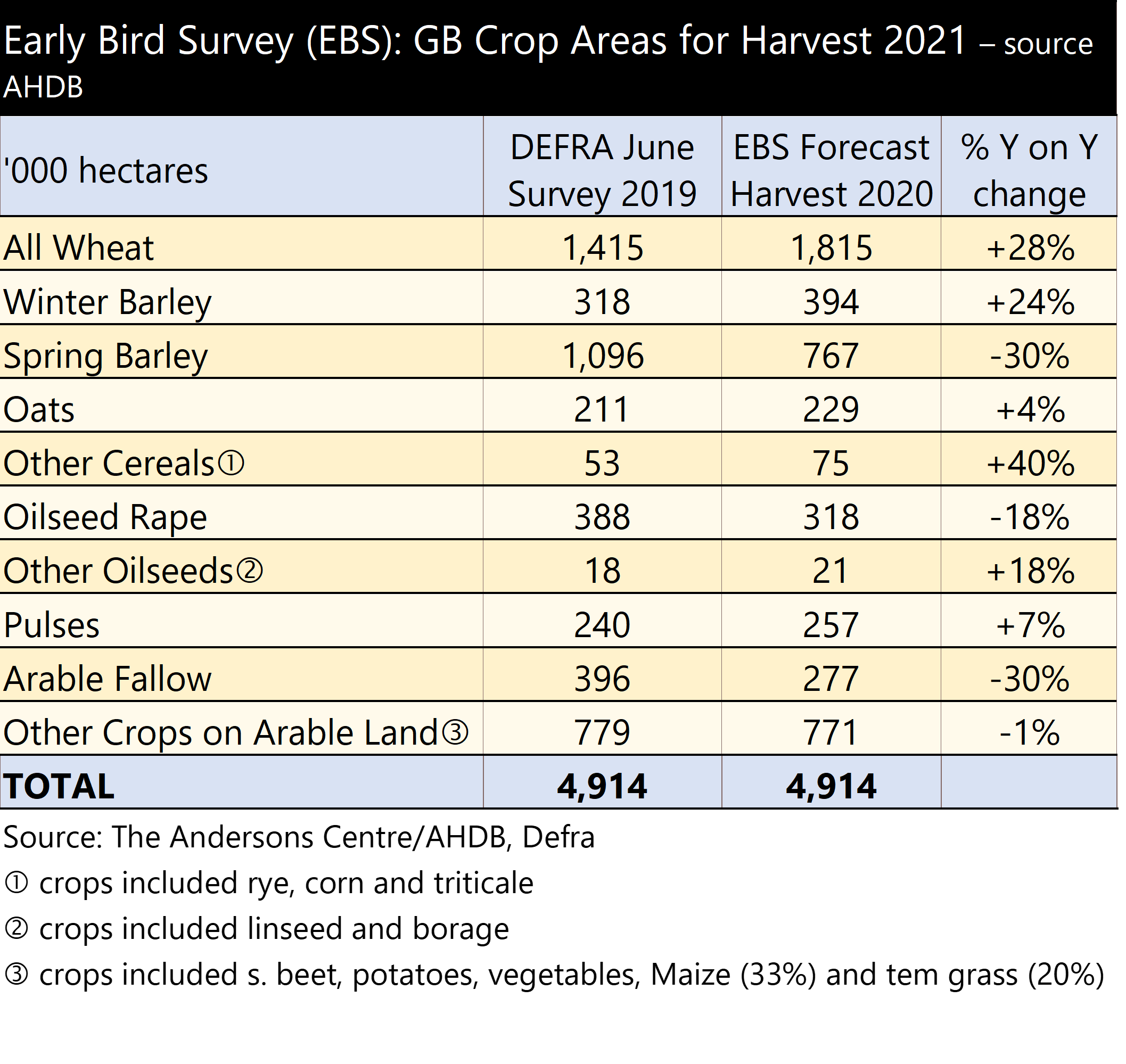

Monthly publications about global crop production and demand at this time of year tend to be rather dull; there are few new crops to report on or harvest progress reports, just a few comments on how much winter crops appear to have been drilled in the Northern hemisphere. These publications only gradually improve the already available data with tweaks here and there meaning price changes are less dramatic than in spring or summer. Statisticians and economists therefore tend to have less of an impact on grain prices than politicians and currency brokers. It is Politics this month that lead the UK market swings. No grain exporters are brave enough to sell consignments of grain that might end up having a prohibitive tariff on it (the tariff is charged at the point of export, rather than the point of sale) so selling for delivery after New Year is a game of commercial roulette. So we await news of a trade deal with Europe which, as the article above points out, is very close to completion, yet potentially miles away. In addition, we also need to know about the Tariff Rate Quotas that could make a dramatic difference, for example to the 1 million tonnes of surplus barley the UK has stockpiled in barns. Over 400,000 tonnes of barley had been exported to the end of October, but this has not continued at the same pace since then due to the uncertainty on the trade rules. The spread between feed wheat and feed barley remains substantial.

The African Swine Fever that swept through China does not appear to have had any affect at all on the demand for soybeans that, it was understood, was fed to the pig herd. China is importing more beans this year than ever before, and that is tipped to top 100 million tonnes, almost two thirds of all global trade. Demand for oils is strong, and with a small oilseed rape crop in the barn and in the ground in the UK, the price has firmed.

The pulse market is relatively thin. This can work in favour of the seller (the farmer) and against. Over the last couple of months, prices have been high, and offered good opportunities for farmers to make high gross margins. But the few buyers have stopped buying and prices have fallen considerably. It could get worse, in some cases in thin markets crops can be hard to move at all. Buyers are now covered until the New Year when they might enter the market again. At least pulses are not really affected by Tariffs, having low rates and exports mostly go outside the EU.