Category: Arable

Sugar Harvest: 2024/25

The sugar beet harvest for the 2024 crop has proved a little disappointing. The average adjusted yield for the 2024/25 season is around 76.5 tonnes per Ha. Clean yields were down due to the poor planting conditions last spring – especially in the Midlands. This was partly offset by higher sugar content. The result does not look too bad compared to the 7-year average adjusted yield of 74.3 tonnes per Ha – but this includes the two very poor years of 2020 and 2022. The sector should be targeting an average much nearer 80 t per Ha.

Pesticides Action Plan

Defra has published its first Pesticides National Action Plan in a decade. It has been developed in partnership between Defra, the Scottish Government, the Welsh Government, and the Northern Ireland Executive. The National Action Plan (NAP) aims to promote the sustainable use of pesticides to minimise impacts on the environment and human health, whilst maintaining food production. The key aim is to reduce the potential harm from pesticides by 10% by 2030. The Plan has three key objectives;

- to encourage the adoption of integrated pest management (IPM) and alternative approaches or techniques

- to establish timetables and targets for the reduction of the risks and impacts of pesticide use, including monitoring and setting targets for the reduction of use of pesticides containing active substances of particular concern

- to strengthen compliance to ensure storage, handling, cleaning and disposal operations do not endanger human health or the environment.

In terms of reducing the potential harm from pesticides, this target is measured using the Pesticide Load Indicator (PLI), which is a UK-specific metric made up of 20 different indicators. The target requires a 10% reduction against each by 2030, using 2018 as a baseline year.

The Plan notes the UK already performs well on pesticide usage relative to the rest of the world, pointing out that whilst the total weight of pesticide active substance applied in agriculture increased globally by around 90% between 1990 and 2020, the UK saw a near 60% decrease over the same period. The full policy paper can be found at https://www.gov.uk/government/publications/uk-pesticides-national-action-plan-2025/uk-pesticides-national-action-plan-2025-working-for-a-more-sustainable-future#annex-3-pesticide-facts-and-figures .

Glyphosate

The Health and Safety Executive (HSE) has extended the use of Glyphosate in Great Britain until at least 15th December 2026. The extension comes following an application by the Glyphosate Renewal Group (GRG) for a renewal of the active substance. The HSE has determined it will not have made a decision on the renewal before the expiry of the licence and, because this is out of the control of the applicant, it must extend the approval period by a further period sufficient to examine the application.

The extension will now allow for a full renewal assessment of glyphosate to be completed. The HSE will consider whether glyphosate continues to meet the legislative approval criteria for an active substance. It has also said this will include a ‘critical consideration’ of the recent European Union (EU) assessment which supported their decision to renew the approval of glyphosate (see https://abcbooks.co.uk/glyphosate-10/). Under the terms of the Windsor Framework, EU plant protection regulations continue to apply directly in Northern Ireland. Therefore the EU’s recent decision to renew Glyphosate permits authorised products to be sold and used in Northern Ireland. Glyphosate has been widely used in agriculture for a number of years now and the loss of it would have a significant impact, particularly now with the rise of regenerative and no-till farming where it is required to control weeds prior to planting.

Potato Market Update

No two potato seasons are the same and that is certainly the case this year. A year ago growers were struggling to plant potatoes in wet and difficult conditions, with some not seeing an end to the planting season until June. This year conditions are much more favourable allowing growers to get onto fields and plant. Soon the cry may be for more water after one of the driest March’s for years.

Despite improved field conditions, growers are unlikely to plant a large potato area. Last year the UK potato area was up a little on the all-time low of 98,000 hectares planted in 2023 to around 100,000 hectares – there are still no definitive Defra figures. A poor growing season meant that the total harvest was around 4.4 million tonnes – the smallest on record. This year, the favourable conditions and two years of much higher prices means growers will probably plant more. However, the area increase is not likely to be above 5%. Average five-year yields of 45 tonnes per Ha would deliver a 4.725 million tonne crop, which would not be much larger than the 2023 crop. It would be remarkable if production nears anything like five million tonnes – before that only weather-affected crops were below that volume – 1976, 1977 and 2012.

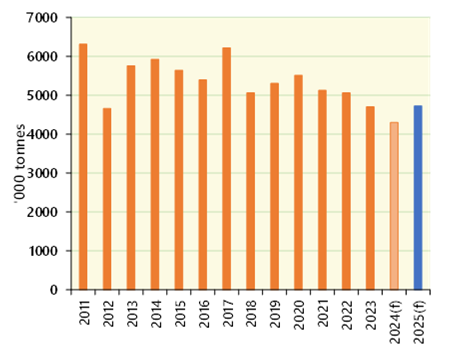

GB Potato Production – Source Defra/World Potato Markets

Prices have eased compared to last year, but they are still historically high. Newsletter Potato Call’s latest report puts Maris Piper prices for packing at up to £350 per tonne. A year ago some buyers were prepared to pay £600 per tonne for the best of the variety.

Whilst prices are lower this season, British growers have not been exposed to the same decline in values that has taken place over recent weeks in mainland Europe. Free-buy prices had reached as high as €300 per tonne for processing potatoes, but lower demand for processed and a spooked market has seen them drop to €175 per tonne in six weeks. Processors in Belgium asked growers to reduce their contracted areas for the 2025 crop, which did not go down well, but hinted at concern among the industry.

Fears of a trade war between processed potato trading nations such as the US, the EU and Canada have affected the market, as has the rise of other suppliers including India, China and Egypt who have seen sales jump by more than 40% over the last year. Lower potato prices in Europe make those stocks more attractive to importers into the British market, given the price difference between the two territories.

Combinable Crops Roundup

Old crop grain and oilseed markets tumbled through March. There is a compounding set of factors behind this, including good planting progress in South America, improved weather in key growing regions, lacklustre domestic demand, and tariffs on Canadian canola (rapeseed) products.

The most liquid old crop UK feed wheat futures contract (May-25) reached a contract low in March at £172 per tonne. Domestically, the strong import campaign this year is going to result in an increase in stocks year-on-year. This is despite a 20% reduction in wheat production in 2024 compared to 2023. Milling wheat premiums have been eroded by the strong import levels. Milling wheat premiums have fallen to just £20 per tonne, compared with £60 per tonne post-harvest.

There is currently a £20 per tonne carry from old crop (May-25) to new crop (Nov-25) futures. With crops reportedly coming out of winter in good condition, with limited disease levels, this premium could come under pressure.

The International Grains Council (IGC) published its first projections of supply and demand for the 2025/26 season on 20th March. It forecasts that wheat carryover stocks will fall by six million tonnes year-on-year, despite an eight million tonne increase in wheat production. For the wider grains complex, a forecast 52 million tonne increase in maize production leads to a one million tonne increase in total grain stocks. The increase in stocks is further underpinned by an eleven million tonne increase in major exporter stocks. This will put pressure on maize prices which is the main cereal crop in terms of global output. There is still a long way to go until the 2025 crops are harvested so there is time for prices to move in either direction depending on crop progress and conditions.

For oilseeds, soyabean stocks are expected to rise marginally, year-on-year (up one million tonnes). However, prices have been undermined by the ongoing ‘trade war’. Following a drawn-out anti-dumping investigation, China has placed 100% tariffs on Canadian canola (rapeseed) oil and meal. Since the beginning of March, the value of Paris rapeseed futures (Nov-25) has fallen considerably. From 3rd to 17th March the value of the contract fell by €40 per tonne (reaching €460 per tonne). Prices have since recovered to €475 per tonne.

Currency is another important watchpoint for the UK market. Sterling has moved stronger against the Dollar. This reduces UK grain prices relative to global markets. However, it also makes imported inputs cheaper. Movements against the Euro have been mixed although the Pound is currently weaker than at the start of the year (supportive of rapeseed prices in the UK).

Fruit & Veg Aid Scheme

Defra has confirmed that the Fruit and Vegetable Aid Scheme will close at the end of this year. The scheme continued funding that was available under the CAP to provide Producer Organisations (POs) in the horticultural sector with support for innovation, collaboration and assistance to market products. It provides £40m per year to the sector through matched funding. The announcement only applies to England, with the administrations in Scotland and Northern Ireland already extending their equivalent schemes. The situation is Wales is unclear, as is the what happens where POs operate across different countries. Defra has stated that it is considering the best way to support horticulture in the future and announcements will be made ‘in due course’. The PO model is widely seen as a success in the horticulture sector. The expectation is that Defra will move to a capital-grants model for any sectoral support in future. This is seen as less flexible and more restrictive than the current system.

Grain Market Update

Old crop UK feed wheat futures prices (May-25) declined through February. There has been little news to support prices for some time. Large opening stocks, high levels of imports and subdued demand will mean the current trend likely continues. The large import levels of milling wheat in particular have reduced the milling wheat premium from an early season peak of £60 per tonne to around £25 now.

Whilst old crop prices have fallen, new crop prices (Nov-25) have increased, driven by rising global grain markets. US maize futures in particular have increased considerably in recent months. Speculative traders (managed money funds) have bought considerable volumes of maize futures, elevating prices. The weather outlook for maize production in both North and South America had been in question, including excess rainfall in Brazil. In the main maize producing region of Mato Grosso, planting of maize is more than eight percentage points behind the five-year average. However, the forecast is for improved weather.

The US weather has also been a key focus. Key wheat producing states in the US have been on the receiving end of temperatures as much as 15C below normal for February. However, this picture is also improving. Additionally, the current market price dynamics for maize and soyabeans in the US is expected to drive an increase in maize planting for 2025. The price gap between old and new crop could close quickly if the funds started selling.

In the short term, there has been support for UK feed barley prices with export demand driving selling opportunities. This has been much-needed owing to the surplus of out-of-specification malting barley adding to the feed heap from harvest 2024.

One positive aspect for arable markets is the strength of the oilseed rape price. That said, the crop area has declined significantly in recent years meaning the price support will only the minority of cereals farmers still growing the crop. In addition, the positive price movement in oilseed rape may not be enough to tempt nervous growers of the crop for 2025 harvest to sell.

A final point worth noting is the direction of fertiliser prices. Natural gas prices, a key input in the production of ammonium nitrate, hit the highest point since October 2023 in February. Prices have fallen back, but remain almost twice as high as the same point last year. So far we have seen an increase in nitrogen prices in the UK market in 2025, but not to the same level as has been observed on the Continent.