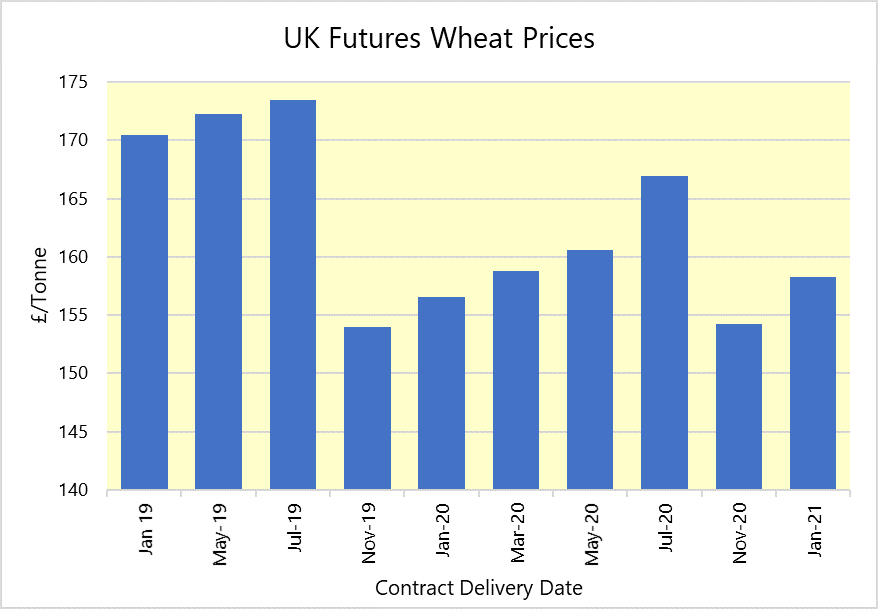

There have been few major fundamentals at play over the last month in the grain markets resulting in small fluctuations. For example, the wheat futures price for May 2019 has fluctuated between £171 and £174.50 per tonne over the whole month, due to various minor factors. This is often the case in the build up to Christmas, when business from millers, maltsters, compounders and other grain users becomes settled, and there are no new surprises in terms of production.

The closure of the two bioethanol plants in the North of England over the last 2 months (reported on in October) means the market place has had to re-calculate the trade balance expectations. Going from a considerable net import requirement for wheat, to a situation of an exportable surplus, impacts UK grain prices and, importantly, logistics. Not only did wheat prices fall, but also, the availability of grain haulage vehicles dramatically rose. The bioethanol plants had been taking large tonnages of grain meaning the haul was, on occasions over long distances, meaning less grain was delivered. Now, the marketplace for hauliers is much looser, and haulage companies have less chance to dictate terms or prices. Where some delivery slots were being missed when the plants were operational, these are now being delivered to.

Before the closure of the Southampton Hovis flour mill (also reported last month), the UK milling industry was, it transpires, considerably over capacity. It seems Hovis may be able to increase its milling volume in its remaining mill in Wellingborough, to still meet some of the contracts it was supplying from Southampton. Furthermore, other firms have some capacity to increase throughput without building any further mills, meeting any other surplus flour demand. We can conclude that the Hovis closure will not affect total UK bread-wheat consumption, whereas the bioethanol plants will affect feed wheat demand.

It is also still not clear whether the Ensus and Vivergo bioethanol plants are closed for good or just for a while. Neither statements were clear, although we understand that the Vivergo plant has taken its staff of 400 down to about 40.

TRADE

China has bought about 60,000 tonnes of French wheat. The volume sold is less relevant than the trade itself. Whilst the business takes some of the EU surplus out of the local marketplace, which is inevitably bullish for EU grains, this is the first Chinese business for EU grains for apparently as much as 5 years. That is more significant, especially as China, according to the International Grains Council and the USDA owns about half of all global grain reserves. It poses questions about the Chinese grain holding strategy and their attitude to purchasing EU grains.

Barley

Very little has happened in the barley market this month either. As Adam Smith pointed out in the 1700’s, when not much interferes with the marketplace of a commodity, its price tends to head towards the lowest cost of production. Perhaps this suggests if you can’t produce it for the current price, note that somebody else clearly can. Last month we reported that barley had, for a while, been higher in value than wheat (which has a higher nutritional value). Barley is normally about 10% lower in value than wheat and this price spread has started to correct itself .

OSR

The oilseed rape market has also been relatively slow, moved more by currency fluctuations than the fundamentals of supply and demand. Note the Southern Hemishphere crop will start going through the combines within a month and might then have an impact on EU values.

Pulses

The very small and poor quality crop from 2018 is not attracting overseas buyers to our marketplace this year. Despite this, Pulses are comparatively well priced compared with other proteins. These two points suggest pulse prices have more downside than upside (compared with the combinable crop benchmark of feed wheat). The low quality and availability of seed means the 2019 crop is going to cover a smaller area than usual for both winter and spring crops.