At this time of year, global markets tend to get somewhat fixated on the weather, in the absence of more concrete information about supply and demand. Quite minor events can have a disproportionate effect on prices. March has seen examples of this.

Grains prices rose in the early part of the month on increasing fears of a drought across the corn belt of the US where precipitation has been low for some months. Then a band of rain swept across the Great Plains and prices dropped back. However, it was then found that the rainfall had not been as widespread as had been hoped, and markets bounced back up again. A similar effect has been seen in Argentina where the soya crop is suffering from a lack of moisture – causing oilseeds prices to firm. Some rainfall during the month caused markets to have a brief wobble but, again, the subsequent conclusion was there had not been enough rain to materially affect the growing crop.

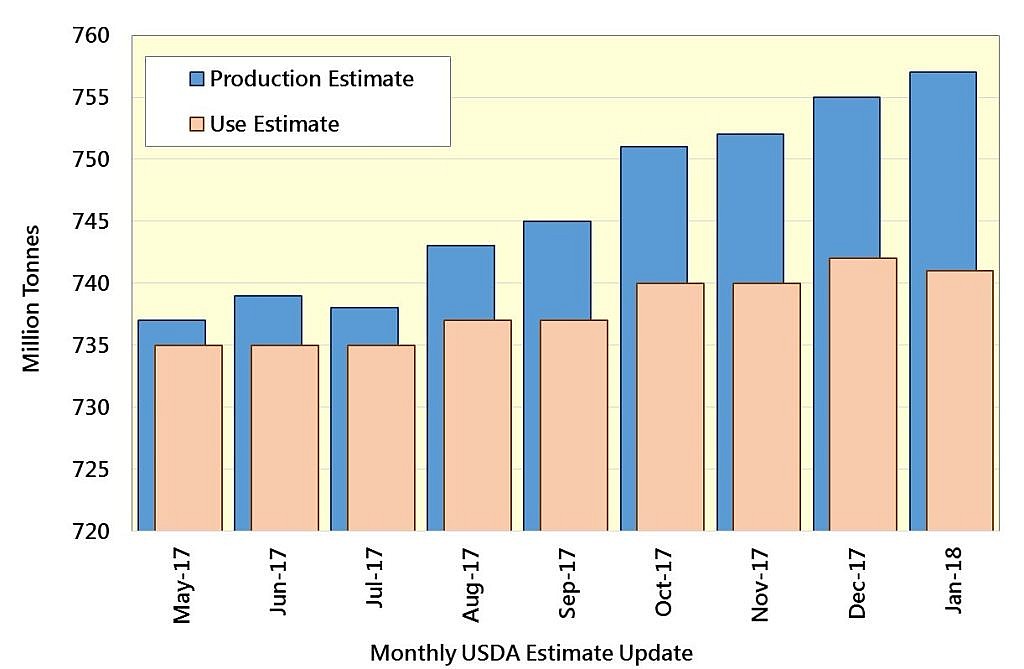

Despites the ups-and-downs, global markets have firmed overall during March. As reported last month, current forecasts for the 2018 harvest show a tightening of supply and demand. The table below shows the latest International Grain Council (IGC) figures. The projected fall in wheat stocks is not large, but the reduction in maize could serve to tighten all grain markets.

| WORLD GRAIN SUPPLY AND DEMAND – Source: IGC (end March 2018) | |||||

| Marketing year – | 2014/15 | 2015/16 | 2016/17 | 2017/18 | 2018/19 |

| UK Harvest Year- | 2014 | 2015 | 2016 | 2017 | 2018 |

| m tonnes | WHEAT | ||||

| Production | 730 | 737 | 754 | 758 | 741 |

| Usage | 714 | 720 | 738 | 742 | 744 |

| End Stocks | 207 | 224 | 240 | 256 | 253 |

| Stocks/Use Ratio | 29.0% | 31.1% | 32.5% | 34.5% | 34.0% |

| Stocks in major exporters* | 66 | 75 | 78 | 66 | |

| m tonnes | MAIZE | ||||

| Production | 1,027 | 984 | 1,088 | 1,045 | 1,052 |

| Usage | 998 | 974 | 1,046 | 1,074 | 1,094 |

| End Stocks | 284 | 295 | 337 | 308 | 265 |

| Stocks/Use Ratio | 28.5% | 30.3% | 32.2% | 28.7% | 24.2% |

| Stocks in major exporters~ | 59 | 81 | 73 | 58 | |

| m tonnes | SOYABEANS | ||||

| Production | 320 | 315 | 350 | 341 | 354 |

| Usage | 312 | 317 | 335 | 347 | 358 |

| End Stocks | 37 | 33 | 47 | 42 | 39 |

| Stocks in major exporters# | 16 | 23 | 19 | 16 | |

| 2017/18 is Forecast, 2018/19 is a Projection. * Argentina, Australia, Canada, EU, Kazakhstan, Russia, Ukraine, US ~ Argentina, Brazil, Ukraine, US # Argentina, Brazil, US | |||||

Closer to home, the prospects for another large Black Sea crop look favourable with good planting conditions reported in Russia and Ukraine. As traditional competitors to the EU for export markets, this could pressure European prices post-harvest if the crop potential is fulfilled.

UK prices have firmed alongside the general global market, but some specific issues also apply. The Pound has strengthened this month as the Brexit negotiations appeared to make some progress (see General/Policy section). UK wheat was already uncompetitive on export markets with very low levels of trade being seen. The shift in currency has made it even more so. Indeed, current relative prices may even encourage imports of grain into the UK. Weighing against this is strong domestic demand, including an upturn in bioethanol production.

On the farm, many drills are poised for action, simply waiting for the soil to dry out to get spring crops in the ground. Although planting is now a two or three weeks behind schedule in many places, it is unlikely that the late spring has shifted planting intentions or potential crop yields enough yet to impact on markets for harvest 2018.