The Government set out measures in the King’s Speech on the 7th November to ban the live export of animals. This would apply to cattle, sheep, goats, pigs and horses for fattening or slaughter. It would not apply to exports for breeding.

Category: Dairy & Livestock

Beef and Lamb Market

Beef

After strong growth throughout the second half of August and September, the prime cattle price has somewhat plateaued through October but remains strong. The deadweight All Steer price for the week ending 21st October was 481.9p per kg, which compares with 437.7p per kg for the same week last year. Prime cattle values still have a little way to go if they are to recover to where they were in May this year (493.9ppkg), but are heading upwards again after sharp declines over the summer period when an upturn in imports impacted prices.

During the first quarter of 2023, UK beef imports were below the previous year’s which, coupled with tight domestic supplies, supported prices through the spring to record levels. However, imports increased through the summer, driven by an upsurge in shipments from Ireland, where cattle prices had fallen, making them more competitive. The price differential between Irish and GB cattle is still particularly wide, with Irish R3 steers trading around an 89p per kg discount to GB steers at the beginning of October. A discount this wide has not been seen since 2015. But UK production remains tight which is supporting prices.

According to the latest Defra statistics, domestic production levels remain below 2022 levels, both in terms of kill numbers and also slaughter weights. Beef production in September 2023 stood at 70,000 tonnes, a decrease of 4% compared with August and down 2% compared with September 2022. Slaughter numbers in September were 1% below year earlier levels, with cow numbers down by 5%. Prime cattle carcase weights have been lighter throughout 2023. September weights were -1.5kg less than in September 2022 at 340kg, this also compares with the 5-year average for September which stands at 342.4kg per head.

Lamb

The prime new season lamb price has remained above year-earlier levels since August. For the week ending 21st October the liveweight SQQ overall price stood at 258.02p per kg compared with 227.28p per kg for the same week in 2022.

In terms of trade, sheep meat imports in 2023 have not followed typical trends. The usual surge in March was much lower this year and, until August, import levels have been historically low. But for the first time this year, in August, monthly quantities of imported sheep meat into the UK were higher than levels recorded a year earlier. More shipments arrived from New Zealand and Australia. The latter is producing record quantities of sheep meat, bringing down their farmgate price and also New Zealand’s, meaning they are very competitive into EU markets. Australia is exporting record quantities of sheep meat this year; this is an area to watch, particularly as domestic supplies usually also start to increase at this time of year.

Having said that, the latest production figures from Defra for September show a 7% decline in volume compared with August, to 22,700 tonnes. This is also 4% lower than for September 2022 and 12% below the 5-year average for September. The drop in production is down to a fall in the number of slaughterings as carcase weights are only 0.1kg per head below last year’s levels. UK clean sheep slaughterings in September dropped 4% on the month to 994,000 head and also 4% on the year. It is not entirely clear why slaughterings are so low, but the good autumn grass growth may have persuaded farmers to keep lambs at pasture rather than look to sell quickly. This would mean more marketings later in the season at, potentially, higher weights.

Dairy Update

UK milk production in September totalled 1,136m litres. This is a 4.5% decline compared to August 2023 and 1.3% below deliveries for the same month last year. This is the first month in the 2023/24 milk year that deliveries have been below year-earlier levels. Cumulative production to date is, however, still ahead of last year, but only by about 0.3%. Some of the drop in September has been attributed to the disruption from milk haulier Lloyd Fraser going into administration during the month, even so, the AHDB are forecasting milk volumes to slow by at least 0.5% over the rest of the milk year and this could be greater if milk prices do not recover.

In terms of prices, UK dairy wholesale markets made some positive movements during October on the back of declining production. All products have recorded an increase in prices. Cream prices have gained by £140 per tonne over the month with both butter and SMP improving by £360 per tonne. Mild cheddar, although recording an increase, this was lower at just £30 per tonne. The recent increases in the GDT have also supported commodity markets. At the two events held in October, the average index has increased by +4.4% and +4.3% respectively and now stands at $3,202 per tonne. The index has increased by 16.9% over the last four auctions and is now over $3,000 per tonne for the first time since July.

With milk production declining and commodity prices increasing, this should alleviate some pressure from farmgate prices, although it might take a couple of months to filter through. Meadow Foods and Barbers Cheese have both announced prices will ‘stand-on’ for November.

Bovine ID Consultation

Defra is inviting views on changes to bovine (including buffalo and bison) identification, registration and movement in England. The current Cattle Tracing System (CTS) was introduced back in 1998 and according to Defra is unable to accommodate any further development. A new system is required to ensure ongoing confidence to consumers, and the international community.

The government’s ambition is to achieve a ‘world-leading Livestock Information Service (LIS)’ while simplifying legislation and supporting new technology. This will allow disease to be identified and controlled more effectively. Working with industry, it aims to put new processes in place to ‘improve the quality of cattle traceability data, and speed at which it is captured’ whilst reducing the administrative burden for keepers, livestock markets, and abattoirs where possible.

The plan is that when bovine electronic identification is introduced, keepers will be able to scan a beast’s ear tag to access its digital record, make changes, and report births, movements, and deaths. This should mean keepers will no longer have to maintain a separate on-farm holding register or manually update passports. Markets and abattoirs will also be able to process electronically identified animals far more quickly without need to cross-reference, or manually update passports.

Defra has said it will be working closely with stakeholders across all parts of the industry to plan the transition to a fully digital service at a pace that suits industry needs.

The full consultation can be found via https://consult.defra.gov.uk/bovine-id-and-traceability-policy-team/changes-to-bovine-identification-registration-and/. Responses need to be submitted by 15th November.

Dairy Update

Domestic milk deliveries continue to run ahead of last year. The AHDB is estimating daily GB deliveries are about 0.8% higher than year-earlier levels, despite falling milk prices. Production is being helped by good grazing. After a difficult start to the season, grass growth has remained healthy throughout the season, although this has not been the case in Northern Ireland, where July and August have been particularly wet, impacting grazing. (Defra monthly production figure are included in Key Farm Facts (KFFs).)

In terms of prices, quite surprisingly the GDT average price index has seen increases at both of the events held in September; the first rises since May. In the auction held at the beginning of the month, it climbed by +2.7%, following a decline of -7.4% at the end of August. In the latest event, held on 19th September, the index increased by a further +4.6% to average $2,957. All products on offer experienced an increase, apart from Cheddar;

- SMP +5.4% $2,400

- WMP +4.6% $2,799

- Butter +3.8% $4,723

- AMF +5.3% $4,787

- Cheddar -1.7% $4,044

UK farmgate prices continue to decline with buyers citing pressure from commodity dairy markets both at home and globally. Announcements from 1st October include;

- 1.6ppl reduction from Wyke Farms, bringing its standard liquid litre down to 36.106ppl

- Meadow Farms has announced a 1ppl reduction, this reduces its standard liquid milk price down to 33ppl

- Barber’s Cheese has also announced a 1.6ppl reduction. This comes after an increase in August which it held for September. This results in a standard liquid price of 35.15ppl

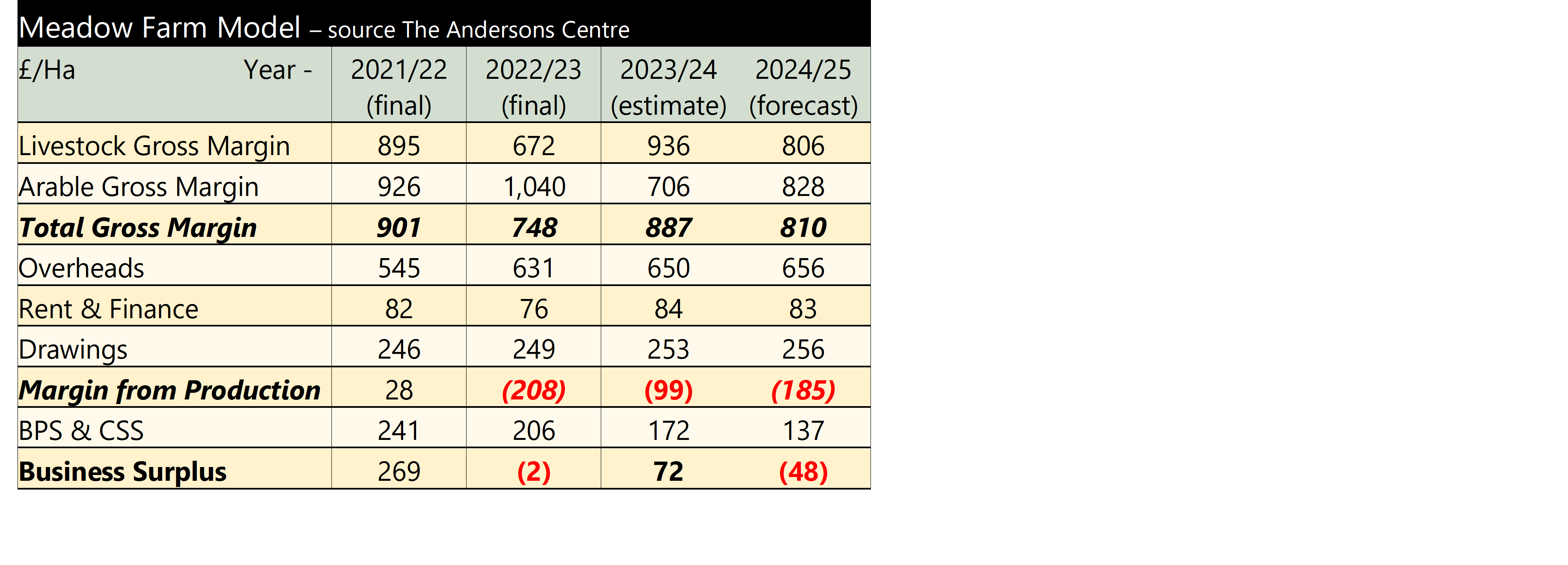

Meadow Farm Update

Meadow Farm has been updated for Anderson’s latest Webinar. An increase in the lamb price since the previous update earlier in the summer means, even though the arable gross margin has declined, the returns for the current 2023/24 year have improved. However, the farm’s margin from production remains negative and with declining subsidy payments the future for the business as it currently operates looks unsustainable.

Meadow Farm is a mixed lowland farm, typical of many livestock holdings in England, it is a notional 154 hectare (380 acre) beef and sheep farm in the Midlands. It consists of grassland, with wheat and barley for livestock feed. There are 60 spring-calving suckler cows with all progeny finished, a dairy bull beef enterprise and a 500 breeding ewe flock.

The table below shows the final results for the last two years, an estimate for 2023/24 and a (tentative) forcast for 2024/25. The 2021/22 year was exceptional as the farm made a margin from production for the first time in many years. For 2022/23, it can be seen how ‘agflation’ impacted even when livestock and crop prices were buoyant. In that year input prices rose substantially and feed costs were especially expensive for this type of holding. The result being the farm made a loss of £208 per Ha from production. A further cut to the BPS meant overall the farm made a loss.

For the current, 2023/24 year, high beef prices and an improved lamb price result in a higher estimated livestock gross margin. Meadow Farm markets its cattle in the autumn and lambs from July through to December. It looked likely that the beef price would have to be adjusted downwards as cattle prices had fallen throughout the summer, but over the last month they have made a strong upsurge. The GB deadweight steer overall price has risen from a year low of 455p per kg in the week ending 12th August to 475p per kg in the w/e 16th September 2023 (see Key Farm Facts). The lamb price has been at similar levels to last year over the summer, but is now tracking above it. The latest GB deadweight SQQ overall figure for the w/e 23rd September 2023 was 553p per kg compared with 525p per kg a year earlier. Whilst lower cereals prices brings down the crop gross margin, the overall gross margin figure is higher than 2022/23. However, overhead costs are drifting upwards and the farm again makes a loss from production, although lower than the previous year.

The budget for the 2024/25 year shows a deterioration in the margin once more – mainly through lower budgeted prices. With another drop in the BPS the farm returns to a loss-making position. Meadow Farm is currently in the Countryside Stewardship scheme. This agreement ends December 2023 and the proprietors are currently drawing up an SFI scheme to start when the CS finishes to see if some of the ‘lost’ BPS can be recouped from this scheme.

Health & Welfare Review

Defra has widened the eligibility criteria for the SFI Annual Health and Welfare Review. Previously it was only eligible to those who had received the BPS. But farmers who have not received the BPS before, as well as those who applied for the Lump Sum Exit Scheme payment, can now apply for the funding to pay for a vet to visit their farm and carry out of a health and welfare review. There is just a minimum number of animals now:

- 11 or more beef cattle

- 11 or more dairy cattle

- 21 or more sheep

- 51 or more pigs

For further details go to https://apply-for-an-annual-health-and-welfare-review.defra.gov.uk/apply/guidance-for-farmers#check-youre-eligible-to-apply This is likely to affect more smaller farmers, but it could also affect some livestock keepers who take land on ‘grasskeeping’ only arrangements and did not claim the BPS.

Dairy Roundup

The Global Dairy Trade (GDT) average index has fallen by -4.3% and -7.4% at the events held in August. The average index now stands at $2,875 compared with $3,768 this time last year. The last time it dropped below $3,000 was in June 2020. WMP and SMP fell by -10.9% and -5.2% respectively at the event held on 15th August. Butter also weakened by 3%, although cheddar experienced a +5.8% rise. The GDT is seen as the bellwether for global markets, meaning domestic prices could well remain under pressure.

Ongoing weak demand from China is influencing world milk markets. Chinese dairy imports started to weaken in 2022 and this trend has continued into 2023. In the first half of 2023, China’s total imports of dairy products stood at 1.39Mt, a decrease of 15.2% year-on-year; this is at a four-year low. The decline is due to a number of reasons including the heatwave the country has experienced, a slowdown in economic growth, zero-Covid policy and an increase in home production. In 2023, China’s milk production is expected to increase by 4.6% compared with 2022 to 41 million tonnes, with WMP increasing by nearly 1.12 million tonnes – meaning demand from China for WMP will be limited. With China being one of the major importers of WMP, they strongly influence global markets, hence the weakness currently being experienced.

In terms of domestic farmgate prices, the Defra UK milk price actually showed a slight increase in July’s price, which stood at 36.11p per litre compared with 36.02p per litre in June. However, this is still over 10p per litre down compared with June 2022. Both Meadow Foods and Barbers have held their prices for September, but Belton Farms has announced a 1ppl cut to bring its price to 36.05p per litre.

UK milk production has eased over the month to record 1,247 million litres in July; 2.2% lower than in June, although 1% more than July 2022 when production was affected by the heatwave. Milk prices and production figures can be found in Key Farm Facts.

OMSCO Rebrand

OMSCO (Organic Milk Suppliers Cooperative) has changed its trading name to Organic Herd. OMSCO is the UK’s largest organic dairy co-op and the rebrand is accompanied by the launch of a premium range of products including cheeses, butter, chocolate and drinking chocolate. CEO Martyn Anthony said the aim is to communicate its values as ‘a producer of the highest quality organic milk and milk products, as well as being a leader in championing the intrinsic benefits of organic dairy’.

Beef & Lamb Markets

Beef

The latest prime cattle prices have recently shown a week-on-week increase after falling for most of the summer. Although prices have been comfortably above year-earlier levels for the whole of 2023, the rises throughout the spring have almost been eroded. Since the end of May, the GB deadweight All-steer price has fallen from 494p per kg for the week ending 20th May to 455p per kg on 12th August. In the week ending 19th August, the price rose by 1.7p per kg on the week, the first rise in 12 weeks. It is too early to say if prices have now stabilised, but why have we seen such a decline?

Domestic demand has fallen due to the cost of living crisis. According to Kantar retail data, volumes of beef sold through GB retail has been below 2022 levels since the start of the year. The unpredictable summer weather as further impacted sales of burgers and grills. Although beef volumes in the food service sector has been positive, this has been more than off set by the decline retail. This picture is similar on the Continent, with consumers reducing spending and this is expected to continue for the rest of the year, according to European Commission forecasts.

The pressure on prices has been further exacerbated by an increase in supply. Not only have UK slaughterings inceased, but imports of Irish beef started to rise in May, following several months of lower volumes. Furthermore Bord Bia is forecasting Irish cattle slaughter to increase in the final quarter of the year. However, overall supplies will be less than in 2022, when the kill was particularly high. But not only have volumes increased, the price of Irish cattle has also fallen, placing downward pressure on UK prices. Irish cattle prices are reliant on the export market and with reduced demand on the Continent (see above) prices have fallen. British cattle usually trade at a premium, but this drop in the Irish price is pulling down GB prices as well. This could affect a recovery in markets into the autumn.

Lamb

The new season lamb trade appears to be stabilising just ahead of last year’s levels, following its seasonal decline. The GB liveweight SQQ for the week ending 19th August was 261p per kg compared with 239p per kg for the year earlier. Similar to beef, domestic demand has weakened as consumers switch to cheaper proteins, but so far this year prices have been supported by export demand. Shipments in the first quarter of 2023 grew by 22% year-on-year. Supplies have tightened on the Continent due to declining production and product from Australia and New Zealand being diverted to the Chinese market. If this continues, domestic prices should remain supported.