Beef

The cattle trade remains buoyant, both for prime and cull animals. Often trade eases after Christmas but this has not been the case so far this year. Strong demand for cheaper, processing meat which is usual in the New Year has seen the cull cow trade hit some exceptional prices. For the week ending the 22nd January the liveweight cull cow price reached 175.28p per kg, over 42p per kg higher than for the same week in 2022. The liveweight prime steer price, after a ‘blip’ in the second week of January, has recovered and in the week ending 22nd January was at 259.22 p per kg; compared to 232.21p per kg in the same week a year earlier. In the deadweight market, prices have risen week-on-week for the first three weeks of the year, starting the year at 449.4p per kg and rising to 455.1 p per kg for the week ending 21st January 2023; some 47.1p per kg above last year’s level.

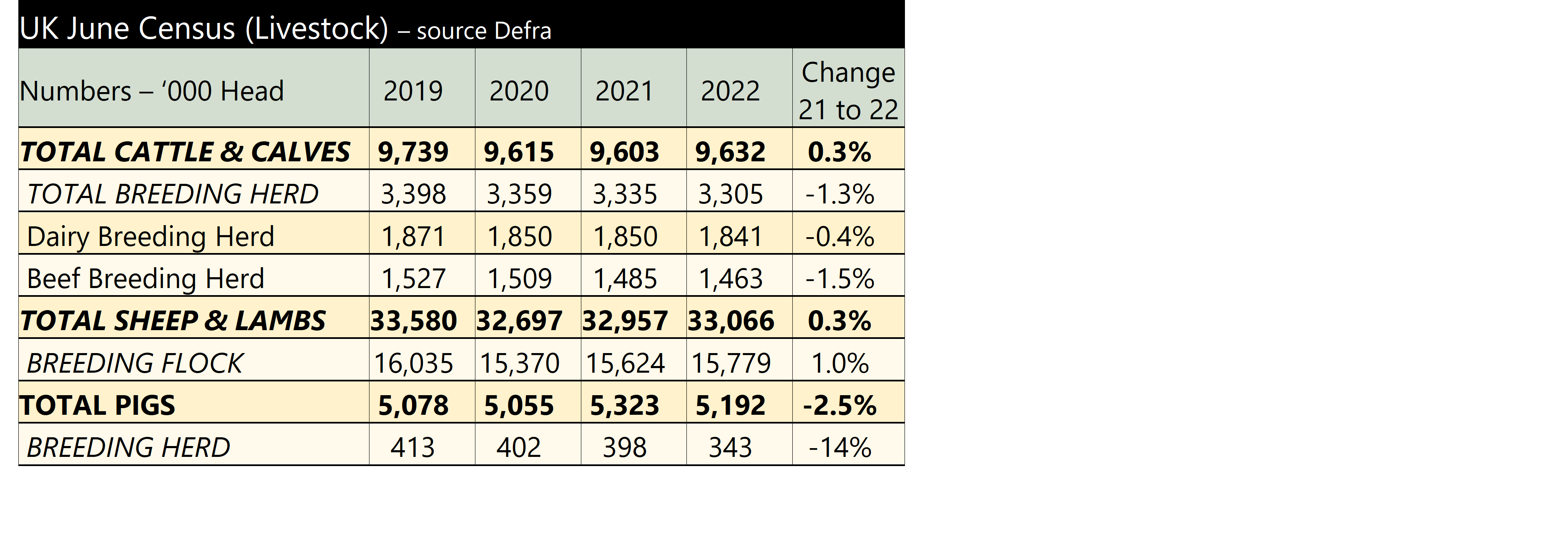

Encouragingly, the strong prices are being achieved even with increased production for the year. According to the AHDB, total beef and veal production for 2022 was estimated to be 906,400 tonnes; up 1.9% (17,000t) on 2021 and just 0.2% below the 5-year average. Prime cattle slaughter numbers were 1.99m head for the year, up 1.5% compared with 2021 (although below both 2020 and 2021 which were just over the 2m head mark). Annual average carcase weights eased by 0.3% to 345.2kg; just under the 5-year average. With high input costs, finishers will have been marketing animals as soon as possible. The cull cow trade has been strong throughout most of 2022, encouraging producers to cull anything old or inefficient. Estimated throughputs for the year totalled 673,700, a year-on-year increase of 5.1% and 1.9% (12,800 head) up on the 5-year average.

Sheep

In contrast to the beef price, prime lamb values seem a little lacklustre, with vendors disappointed with prices. Markets fell back below year-earlier levels in the autumn. They did experience a rise in December, but never reached the highs of 2021, with GB SQQ liveweight price topping the month at 251.3p per kg in the week ending 24th December, compared with 285.5p per kg for the year earlier. Although this may seem disappointing, the lamb price has been increasing for a few years now and although 2022 prices were lower than 2021, it still remains 33p per kg above the five-year average. The problem is that it has fallen at a time when costs have increased. What happens over the next few weeks will be telling. As is often the case, prices have fallen post-Christmas with the liveweight SQQ for the week ending 21st January at 236.74p per kg compared with 263.89p per kg in 2022.

In terms of production for 2022, it is estimated to have been 275,800 tonnes. This is a 3% increase on 2021, however this compares to 296,100 tonnes and 307,500t in 2020 and 2019 respectively and is 6% below the 5-year average. Carcase weights have remained stable at an average of 20.2kg, meaning throughputs have increased on the year. The number of clean sheep slaughtered is reported to have been 12.1 million head, up 3% on the year, although down 6% compared with the 5-year average. Cull sheep slaughter numbers are also up on the year by 1.2m head (4%) but down by 19% on the five year average.

With the main lambing season coming-up anecdotal evidence is suggesting that the drought last summer may have taken its toll on some ewes and shearlings. Results from scanning indicate lambing numbers may be lower than usual.

The economic climate for pig producers is currently hugely challenging and this is shown in the large reduction in the breeding herd. Total pig numbers, although down by 2.5% on last year, are still high. This is due to the figures including pigs which were having to remain on farm due to problems in the processing sector. We could see even further contraction of the pig breeding herd unless circumstances improve. The full Survey results can be found at

The economic climate for pig producers is currently hugely challenging and this is shown in the large reduction in the breeding herd. Total pig numbers, although down by 2.5% on last year, are still high. This is due to the figures including pigs which were having to remain on farm due to problems in the processing sector. We could see even further contraction of the pig breeding herd unless circumstances improve. The full Survey results can be found at