Production

GB milk production for June was already 2% lower than year earlier levels even before the heatwave in mid-July which will have impacted production further. According to AHDB data, GB deliveries fell by 8% between May and June, but are still in line with its (updated) seasonally forecasted drop in production. Cumulative production for the season so far (April to June) stands at 3,283m litres, also 2% less than at the same point in 2021. Daily deliveries for the week ending 16th July show a 1.7% decline on the week, but this is expected to get larger due to the extreme weather conditions during mid-July. Not only will heat stress have impacted production, but going forward, grass growth and quality has been affected. Despite the strong milk price, high input costs are not encouraging producers to increase their yields.

Furthermore, the AHDB reports the global picture to be very similar. Deliveries for May record a year-on-year decline with little change expected for the rest of 2022. Latest forecasts for the key producing countries show a 0.5% decline in production for the year. The EU is forecast to experience the largest decline, in terms of volume, down by 838m litres compared to 2021 levels. Similar to GB, the hot, dry weather on the continent and increased feed costs are impeding production.

In Australia and New Zealand, even though they haven’t reached their seasonal peaks in production, they are forecasting year-on-year declines of -2.4% and -0.7% respectively after such poor starts to the year. The US is forecast to see a small decline. Bucking the trend is Argentina, which is the only country to be forecasting year-on-year growth, although at a slower rate than last year, as rising costs start to have an impact.

Prices

The tight supply situation continues to support dairy prices and further UK farmgate price increases have been announced including confirmation from Freshways that it will be paying its suppliers 50ppl from 1st September. However, Promar’s monthly review of the cost of production (COP) for the Müller-Tesco Sustainable Dairy Group (TSDG) has shown a 0.32ppl reduction. In somewhat of a surprise, reports suggest the cut is mainly due to a reduction in feed costs. However the understanding is producers will still receive 46ppl, the same as the Müller Direct price for August.

Interestingly, the Global Dairy Trade (GDT) index has seen big falls at the last two events, by -4.1% and a further -5% at the latest event held on 19th July. The average index now stands at $4,166/t. The index has fallen in 8 of the last 9 events. There appears to be downward pressure on most commodities, but with the supply situation so tight and spot milk in the UK at 55p – 60ppl, farmgate prices continue to be supported.

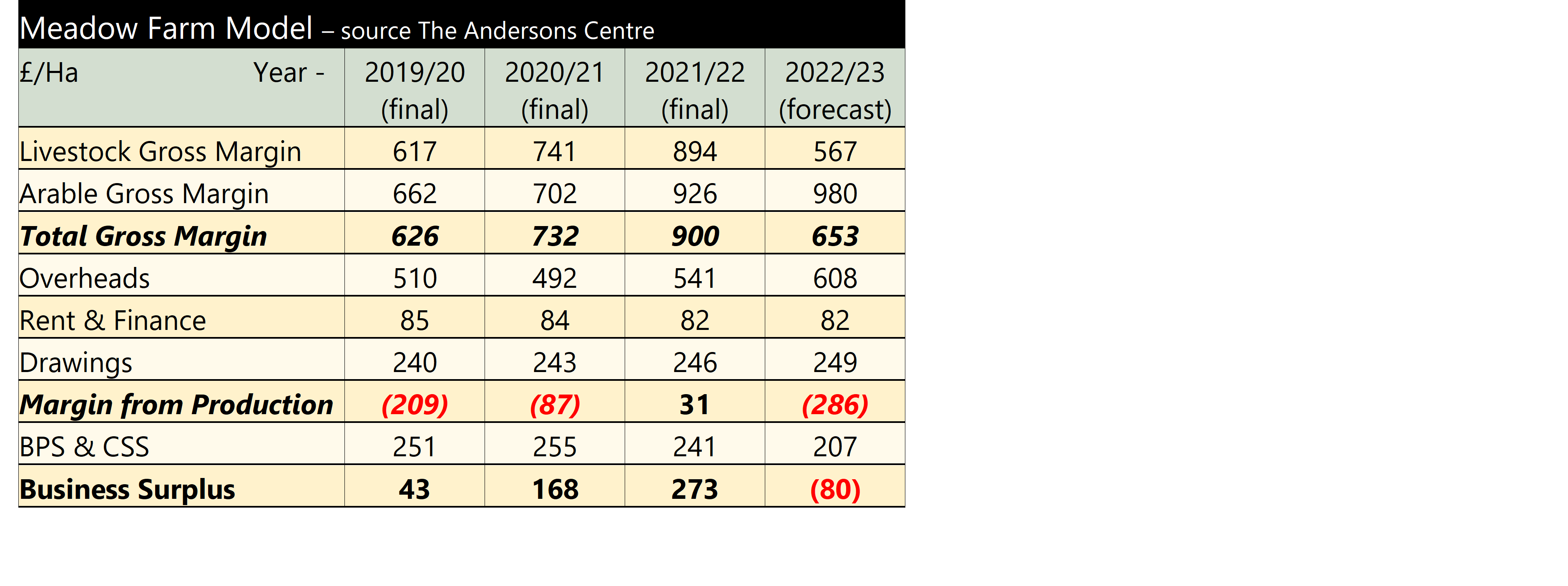

The final column is a forecast for 2022/23 and it clearly shows the impact of increased, fuel, fertiliser and feed costs for this type of farm. Currently, the UK beef price is running ahead of last year’s levels and prices have been ‘tweaked-up’ in the current budget. However, some caution has been exercised. Meadow Farm markets its beef cattle from August to October and an increase in supplies, particularly from Ireland could lower prices by then and this has been accounted for in the budget. In addition, as the energy crisis hits home and consumer spending power is affected, this could see consumers switch to cheaper proteins. However, in lock-down, when consumers were forced to eat at home, the UK beef and lamb market did well. So, if hard pressed consumers reduce their out-of-home consumption, this may not impact as much as might be feared. Overheads rise due to increased fuel prices. A planned investment in a new cattle shed, to replace old ones, means the depreciation increases. The result is the margin from production plummets and not even the BPS, (which is reduced by 20% this year) can bring the Business Surplus back into the black.

The final column is a forecast for 2022/23 and it clearly shows the impact of increased, fuel, fertiliser and feed costs for this type of farm. Currently, the UK beef price is running ahead of last year’s levels and prices have been ‘tweaked-up’ in the current budget. However, some caution has been exercised. Meadow Farm markets its beef cattle from August to October and an increase in supplies, particularly from Ireland could lower prices by then and this has been accounted for in the budget. In addition, as the energy crisis hits home and consumer spending power is affected, this could see consumers switch to cheaper proteins. However, in lock-down, when consumers were forced to eat at home, the UK beef and lamb market did well. So, if hard pressed consumers reduce their out-of-home consumption, this may not impact as much as might be feared. Overheads rise due to increased fuel prices. A planned investment in a new cattle shed, to replace old ones, means the depreciation increases. The result is the margin from production plummets and not even the BPS, (which is reduced by 20% this year) can bring the Business Surplus back into the black.