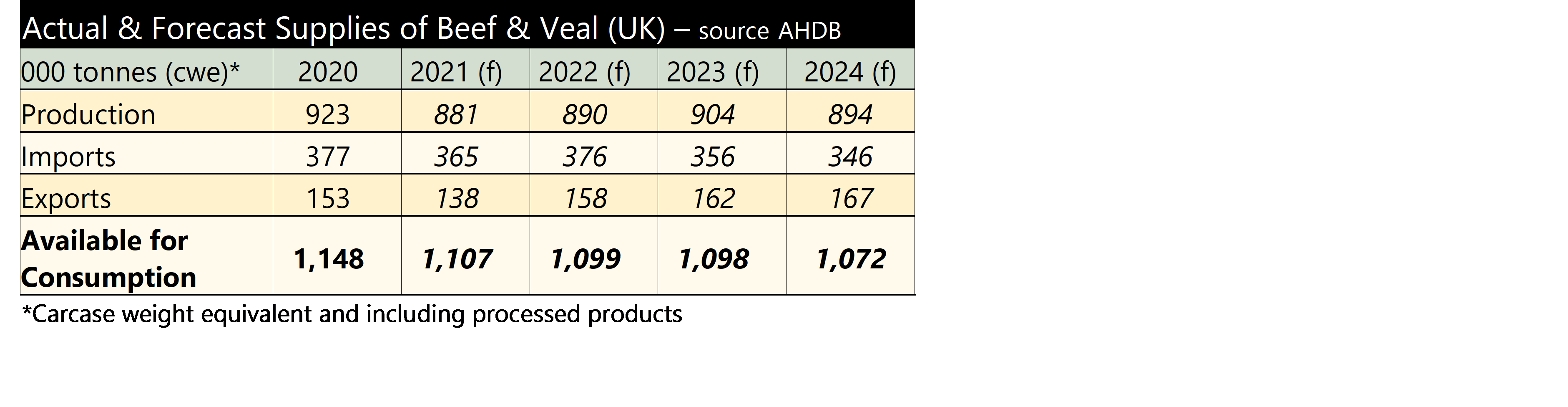

The AHDB has released its latest outlook for the UK’s beef sector. The beef market has experienced some exceptional prices in 2021 which have continued into 2022. Tight supply and strong retail demand has driven prices. But even so, higher feed, fertiliser and fuel prices are impacting on profitability.

The AHDB is forecasting a 1% increase in total beef production in 2022. The UK prime cattle slaughter is expected to grow by 2%, but this is forecast to be offset by around a 1% fall in the slaughter of cull cows. Prime beef supplies are expected to remain tight in the first half of 2022, but increase in the second half of the year. In 2023, production could see further ‘moderate’ growth due to changes in dairy bull calf management. An increase in beef semen used on dairy cows will result in more ‘beef-type’ cattle coming from the dairy herd, contributing to the total production.

Beef consumption has performed well throughout the pandemic. It experienced the fastest volume increase in retail of all the meat proteins in the 52 weeks ending 14th June 2020. However, it did return to slightly more normal levels in 2021, reducing by 6% on the year. However, compared to 2019 levels retail sales remain strong; up by 4%. Foodservice conditions remained difficult in 2021. The AHDB estimates the eating-out market for beef in the 52 weeks ending 26th December 2021 declined by -5% year-on-year and this follows a -54% fall in 2020. Deliveries and takeaways however, continue to perform well. The AHDB estimates beef volumes in this market rose by a further 40% in 2021 year-on-year, meaning an 87% increase compared to pre-pandemic levels (2019). However, this increase is not expected to be enough to offset the decline in beef consumption from eating-out and retail, meaning total beef consumption for 2021 is estimated to be 4% less than 2020 and the same as in 2019.

In 2022 the AHDB is forecasting total beef consumption to be down by a further -1% compared to 2021 (and 2019 levels). This is mainly through a continued drop in retail sales. Inflation and, in particular, the increase in energy costs is expected to impact on household finances and therefore purchases. The food service sector is expected to start to see a recovery, especially through the second half of 2022.

Looking at trade, the AHDB forecasts imports to grow by about 1% in 2022 compared to 2021. The first quarter should see a year-on-year increase as imports last year were affected by Brexit. Ireland, the UK’s biggest supplier of beef, could see a 3% increase in cattle numbers and with its prices at a discount to the UK, imports are expected to be attractive, especially for the food service sector. Exports are forecast to grow by 10% as demand from the foodservice sector on the continent increases, as it continues to open up after Covid and, at the same time, production across the EU and more widely in North America and New Zealand is forecast to remain tight. Lower global supplies should support EU prices which in turn should maintain UK values. But increased demand from the food service sector which often uses cheaper imports together with an increase in lower priced Irish beef could exert some downward pressure on UK prices.

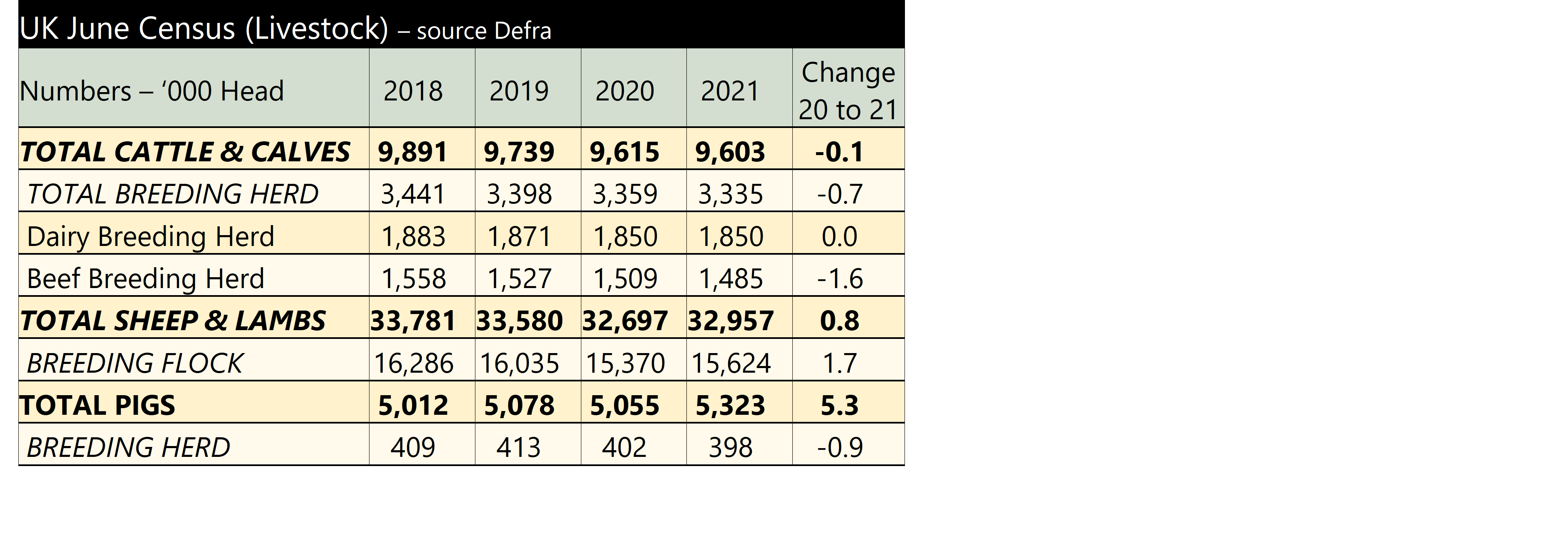

Although the pig breeding herd has experienced a decline, total pig numbers have increased by 5.3%. This is likely to be as a result of producers having to keep pigs on farm longer than normal due to a reduction in the processing facilities experienced this year, rather than a fundamental increase in production. The economic climate for pig producers is currently very challenging and we could see a further contraction of the breeding herd unless circumstances improve. The full Survey results can be found at

Although the pig breeding herd has experienced a decline, total pig numbers have increased by 5.3%. This is likely to be as a result of producers having to keep pigs on farm longer than normal due to a reduction in the processing facilities experienced this year, rather than a fundamental increase in production. The economic climate for pig producers is currently very challenging and we could see a further contraction of the breeding herd unless circumstances improve. The full Survey results can be found at

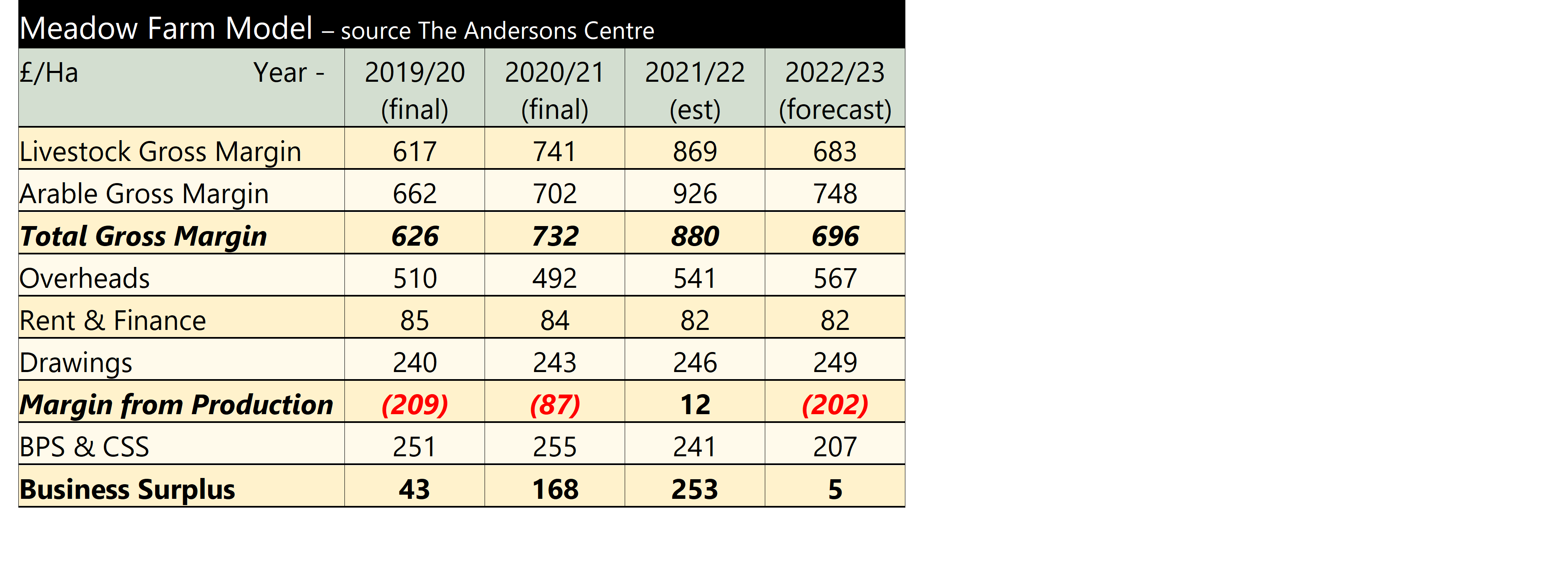

The final column is a forecast for 2022/23. Livestock prices are expected to drop back as supplies start to increase, likewise arable prices and yields are expected to be more ‘normal’ but fertiliser costs have increased. Overheads rise due to increased fuel prices and the proprietors are planning to invest in a new cattle shed, to replace old ones, meaning the depreciation increases. The result is the the margin from production is back to 2019/20 levels but with the BPS reduced by 20%, the business surplus is very small. The proprietors of Meadow Farm are keeping an eye on the new Sustainable Farming Incentive, to see if some of the ‘lost’ BPS can be recouped from this scheme.

The final column is a forecast for 2022/23. Livestock prices are expected to drop back as supplies start to increase, likewise arable prices and yields are expected to be more ‘normal’ but fertiliser costs have increased. Overheads rise due to increased fuel prices and the proprietors are planning to invest in a new cattle shed, to replace old ones, meaning the depreciation increases. The result is the the margin from production is back to 2019/20 levels but with the BPS reduced by 20%, the business surplus is very small. The proprietors of Meadow Farm are keeping an eye on the new Sustainable Farming Incentive, to see if some of the ‘lost’ BPS can be recouped from this scheme.