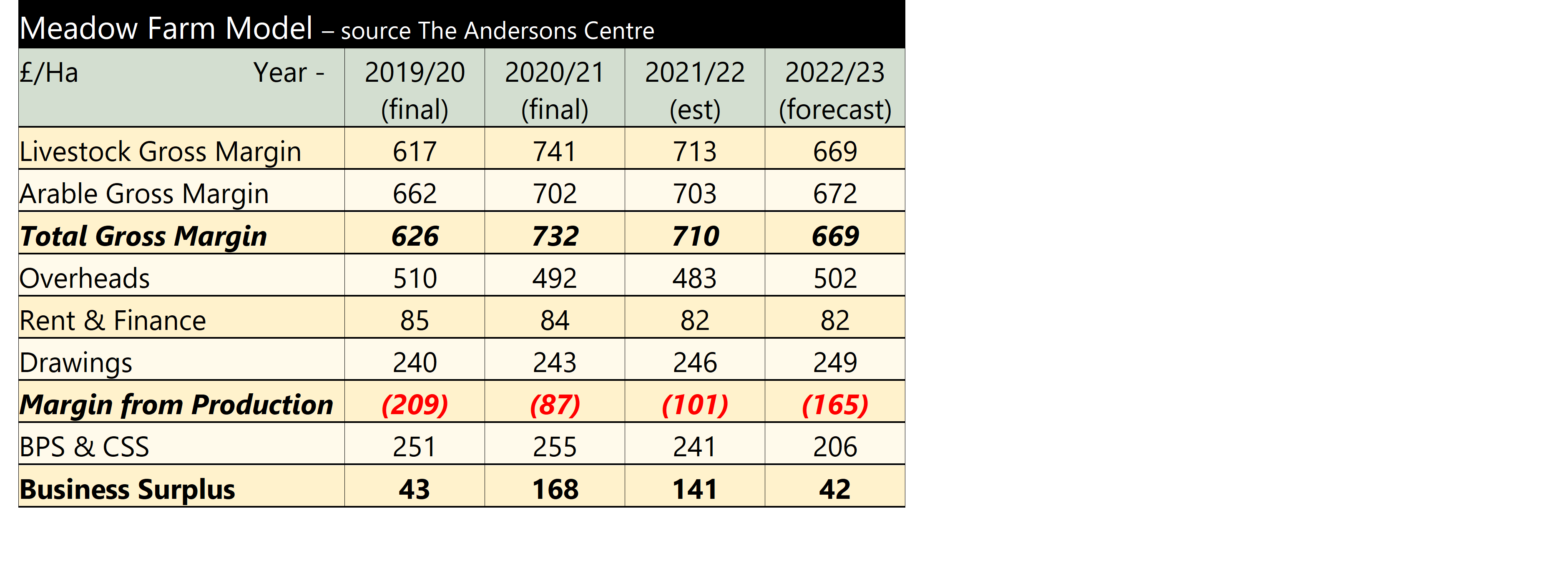

The Andersons Centre’s mixed lowland farm model ‘Meadow Farm’ has been updated. The table below shows the final results for 2019/20 and 2020/21, and an estimate for the current year, and an early forecast for 2022/23.

The 2019/20 year was affected by low livestock prices, particularly for beef. But the beef price recovered throughout 2020 and is currently very strong. The lamb price also continued to perform well throughout the year and with a Free Trade Agreement (FTA) negotiated with the EU, prices this spring have exceeded expectation. Meadow Farm sells all its finished cattle from August to October and lambs from July, with all having left the farm by the end of December. Therefore, it didn’t fully capitalise on the very high lamb prices seen in the first quarter of 2021. Even so, as the table shows, the livestock gross margin in 2020/21 was the strongest it has been for some time. After a tough winter and spring, it looked like the arable results from harvest 2020 would be poor. However, as a result on the rise in crop prices seen through autumn 2020 the gross margin strengthened. Overheads fell, in part due to a drop in the fuel price, but also because of a decline in machinery and property depreciation. With such a poor year in 2019/20 the proprietors of Meadow Farm did not invest in any big pieces of machinery. But such low levels of reinvestment are not sustainable. The result being the combined margin from production for 2020/21 is the strongest it has been for a number of years, however the margin from production is still negative and it still takes the BPS and CSS payments to provide profit.

Looking ahead to the rest of the current 2021/22 year, livestock prices are expected to remain good, but not quite at the levels of 2020/21, especially the lamb price. The arable gross margin is budgeted to remain pretty similar as a drop in crop price is compensated by better yields. Overheads reduce, due to lower machinery depreciation, but some of the machinery will soon need replacing. The margin from production is not as good as 2020/21 but is still better than recent history. 2021/22 is the first year of the Agricultural Transition and the BPS is reduced by 5%, but the addition of this still leaves a good profit for the business relative to other years.

The final column is the first (tentative) forecast for 2022/23. Livestock prices are expected to drop back further, likewise arable prices and yields are expected to be more ‘normal’. Overheads rise due to increased fuel prices and a small machinery purchase means the depreciation increases. The margin from production is not as good as the last couple of years and the BPS is reduced by 20%, meaning the business surplus is back to 2019/20 levels. The proprietors of Meadow Farm are keeping an eye on the new Sustainable Farming Incentive, to see if some of the ‘lost’ BPS can be recouped from this scheme.

Meadow Farm is typical of many livestock holdings in England, it is a notional 154 hectare (380 acre) beef and sheep farm in the Midlands. It consists of grassland, with wheat and barley for livestock feed. There are 60 spring-calving suckler cows with all progeny finished, a dairy bull beef enterprise and a 500 breeding ewe flock. The business is subsidy-dependent, but with direct payments decreasing from 2021 it will need to adapt; maybe through restructuring to reduce its overheads, which are fundamentally too high, or perhaps by taking advantage of the new ELM scheme, or possibly a combination of both.

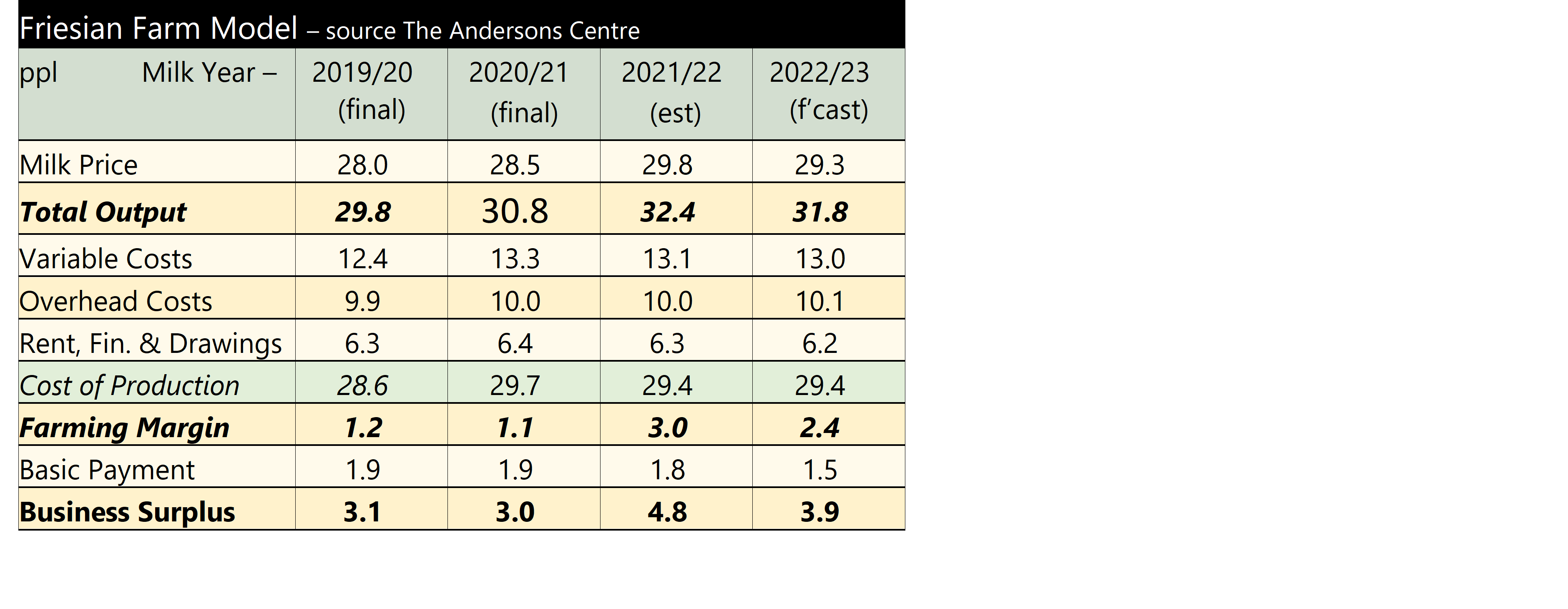

The 2019/20 year showed a recovery in profitability after the drought-hit 2018/19, even though the milk price was weaker. Farmgate prices firmed slightly for 2020/21, however variable costs rose – in particular feed, following the poor harvest of summer 2020.

The 2019/20 year showed a recovery in profitability after the drought-hit 2018/19, even though the milk price was weaker. Farmgate prices firmed slightly for 2020/21, however variable costs rose – in particular feed, following the poor harvest of summer 2020.