The end date for Defra’s ‘Call for Views’ on possible future measures to accelerate bovine TB eradication in England has been extended to 21st April 2021. The deadline for responses to the current consultation on bovine TB remains 24th March 2021. See article of 10th February for details of the Consultation and the Call for Views.

Category: Dairy & Livestock

Dairy Markets

At the latest Global Dairy Trade (GDT) auction, the price index continued to perform well, increasing by 3% to average $3,746. It is now 24% higher than at the low point in April last year and has increased in 10 out of the last 11 events. At the last auction on February 16th, all products on offer realised an increase;

- WMP – +4.3% to average $3,615 per tonne

- SMP – +0.3% to average $3,207 per tonne

- Cheddar – +2% to average $4,268 per tonne

- Butter – +2% to average $5,129 per tonne

- AMF – +1.1% to average $5,527 per tonne

- Lactose – +0.4% to average $1,232 per tonne

Closer to home, domestic farmgate milk prices are easing, with some reductions being announced, particularly for the the middle ground liquid processors who are being hit by school closures and limited food service demand during the third lockdown. However, plenty of processors are holding their prices until at least 1st April including;

- Graham’s Dairy

- Belton Farm

- Barbers

- Crediton Dairy

- First Milk Members’

- Saputo

Liquid processors, Paynes Dairies has announced a 0.5ppl reduction from to 1st February. Similarly Pensworth dairies has been forced (due to Covid) to reduce it’s price by 1ppl from 8th February. Suppliers to Freshways have been given a month’s notice that their price will be reduced from between 0.5ppl and 1ppl from 1st March, but with the market changing rapidly under lockdown it is unable to confirm the the exact amount at present. Medina has also announced a 1ppl milk price reduction from 1st March. It is likely downward pressure on prices will continue in the short term as the pandemic continues to impact on the supply/demand balance, but longer term with lockdowns easing it is hoped this will diminish.

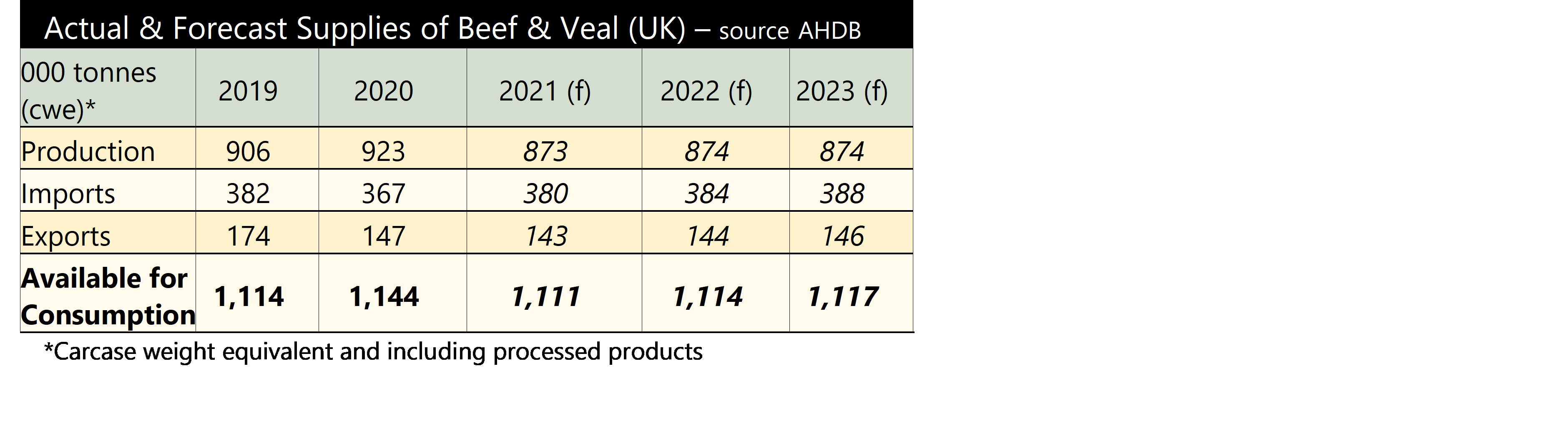

Beef Outlook

The prime farmgate beef price continues to perform well. Deadweight values are in the region of 45ppkg more than at the same period last year and about 35ppkg higher than the 5-year average. It is a similar picture for the cull cow trade. For both categories, prices for poor specification cattle fell a little over the fortnight to 6th February, but for higher specification cattle, the prices have continued to strengthen; highlighting the need to hit specification. But what can be expected going forward?

The AHDB has released its latest Market Outlook and is forecasting a 5% reduction in production in 2021, with domestic consumption falling by 3%. Imports are expected to grow by 4% together with a 3% decline in exports, both mainly due to lower domestic production.

Production

Production

The AHDB is forecasting prime cattle slaughter to decline by 5% year-on-year to 1.95m head. According to BCMS figures the number of prime cattle (aged 12-30 months) was 5% less in October 2020 compared to year-earlier levels. Added to this, strong prices in 2020 saw producers drawing cattle forward early, resulting in prime cattle slaughter numbers finishing the year 2% up when a decline was expected. Therefore, supplies for 2021, particularly in the first half of the year, are expected to be tight. Carcase weights have been steadily declining over recent years and this is expected to continue, particularly if prices remain strong, encouraging producers to finish cattle quicker and at lighter weights. High feed prices will add to this trend.

Trade

Beef imports are forecast to rise by 4% in 2021. Demand from the food service sector is anticipated to increase as lockdown ends and, although consumption is expected to decline, this will not be enough to offset the drop in domestic production and imported beef will be used to make up the shortfall. However, imports may also be limited by tighter Irish supplies, especially in the first half of the year. Lower domestic production will result in exports declining again. The AHDB is forecasting a 3% reduction as trade friction at the borders due to Brexit and disruption in the food service sector in Europe, due to Covid-19, also affects exports.

Consumption

Beef has faired pretty well during the pandemic after the initial carcase balance problems. It has seen the greatest volume increase in retail of all the proteins during the Coronavirus outbreak. According to market research company, Kantar, for the w/e 27th December beef retail volumes were up by 11% on the year. The largest growth was for mince, burgers and steaks. However, the out-of-home market for beef fell by 56%, although delivery and takeaway volumes of beef rose by 28%.

Price Outlook

Tighter domestic and Irish supplies should help maintain the current strong prices in the short term. Last year also showed higher retail demand supporting prices whilst the food service sector was restricted. The greatest question appears to be whether consumer demand will remain robust if 2021 sees the full economic effect of Covid hit home. Even if consumers continue to buy beef, they may switch to cheaper cuts, causing carcase balance issues once again which could lead to downward pressure on prices.

Bovine TB Consultation

A new consultation on the next steps to eradicate bovine TB has been launched. It is seeking views on plans which include the phasing-out of intensive badger culling after 2022. The eight week consultation which can be found at https://consult.defra.gov.uk/bovine-tb-2020/eradication-of-btb-england/ .

The paper is asking for responses on a range of proposals (see below) but the most controversial is the plan to stop issuing intensive cull licences for new areas after 2022. The strategy would also enable any new licences to be cut short after 2 or 3 years based on a review of the latest scientific evidence at the time. Any new supplementary cull licences (which are issued in regions after intensive culls are complete) would be restricted to just two years and would not be regranted again. Many will be disappointed with this, especially as the statistics show an improvement in the incidence of TB breakdowns and numbers of animals needing to be culled. But the phasing-out of badger culling and replacing with vaccination and surveillance was among the Government’s three top priorities in response to the Godfray review in March 2020. Other proposals in the consultation include;

- Extending Post-Movement TB testing to parts of the Edge Area

- Use of the Interferon-gamma test in the High Risk Area and Edge Area

As bovine TB policy is devolved, the consultation is England only, responses need to be made by 24th March 2021. In parallel to the consultation Defra is also conducting a ‘Call for Views’ on further ideas, these include;

- Changes and improvements to TB testing

- Incentivising increased uptake of biosecurity measures

- Supporting responsible cattle movements

- Rewarding low risk purchasing behaviour

Further information can be found via https://consult.defra.gov.uk/bovine-tb-2020/bovine-tuberculosis-call-for-views-on-possible-fut/ . Similar to the Consultation, views need to be made by 24th March 2021

Milk Contracts

The Government is to introduce statutory regulation of dairy contracts. This follows the consultation launched last June which explored the imbalances of power within the supply chain and, in particular, where milk buyers are able to modify the terms of the contract with little or no notice. The Government has stated that it is ‘clear there is a need to introduce new regulations to require certain standards for contracts between those producing and buying milk for processing’. It also recognised that the ‘distinctive’ circumstances in Northern Ireland may need to be reflected in the regulations.

A voluntary code of practice on dairy contracts was introduced in 2012. However, with a (small) number of processors continuing practices such as backdating price cuts or giving little or no notice of contract term changes, it has been decided that more robust measures are required. The farming Unions have been campaigning for regulation to be put on a statutory basis for many years.

Defra will now work with the devolved administrations to develop a new statutory Code of Conduct for the sector using Section 29 of the Agriculture Act 2020 – Fair Dealing Obligations of Business Purchasers of Agricultural Products. The new Code will establish minimum standards but with the ‘flexibility to adapt to individual circumstances’. It is acknowledged that further work and engagement with the industry will be necessary before the new Code is drawn up.

Dairy Roundup

Prices

The GDT average price index, often seen as the bellwether for the dairy markets, has seen strong improvements at both events held in January. At the auction on 5th January 2021 the average price index was up by 3.9% and rose a further 4.8% at the latest event held on 19th January to close the month at $3,593. Only cheddar experienced a small drop, by 0.3%; SMP and WMP rose by 7% and 2.2% respectively, with butter up by 4.6%. SMP is now at $3,243 per tonne, the highest value for the last five years. Anhydrous Milk Fat (AMF) saw a 17.2% increase. The index has risen at every event now since the end of September 2020, except for one at the end of November. This is despite Covid-19 impacting the demand from the food service sector, but recently there has been a weakening of the US dollar making products cheaper which looks like it has more than offset the lack of demand due to Covid disruptions.

This positivity is also reflected in domestic farmgate prices, which according to Defra’s latest release were averaging 30.38ppl in December (See Key Farm Facts). And this looks set to continue, with a number of processors announcing prices will be maintained until at least March, these include; First Milk members, Arla members, Credition Dairy, Saputo, Barbers and Belton Cheese. As a result of the Tesco cost tracker review, Tesco aligned suppliers will receive a 0.4ppl increase from 1st February and suppliers to the Co-op Group will also see a rise from the beginning of February of 0.22ppl.

Production

The AHDB is forecasting global milk production to rise by around 1% in 2021, increasing total supplies by 3.1bn litres. This is at a slower rate than 2020. Despite disruptions to Coronavirus it is expected deliveries increased by just under 4.9bn litres in 2020, up by 1.7% compared with 2019.

Meanwhile, the EU is forecasting milk production in the EU-27 to increase by 0.6% per annum, reaching 157bn litres in 2030. This is the forecast in the EU Commission’s latest Agricultural Outlook 2020-2030. The full report can be found via agricultural-outlook-2020-report_en.pdf (europa.eu). The growth in production is less than in recent years due to a reduction in estimated herd size and a lower yield growth (1.4% per annum). According to the report, this is because non-conventional systems are expected to experience an uptake in response to consumer demands for sustainability and the environment; the share of organic milk is expected to grow from 3.5% to 10% by 2030.

Meat Market Update

Beef

Prime cattle prices have started the New Year strong. For the week ending 16th January 2021, all deadweight price categories recorded an increase. The R4L steer price increased by 6p per kg on the week with the all-prime price rising by 5p to average 376p per kg. This measure is now 46p above last year’s level for the same week and 33p above the five-year average. In 2020, the price started the year at a 5-year low and ended at a 5-year high. The cull cow market has also made a strong start to the year, with the deadweight price rising by 9p per kg on the week. According to British market research company, Kantar, in the last 12 weeks to 27th December 2020, total spend on beef was up 12.8% year-on-year to £1.1bn and volumes grew by 9.7%. All beef products have seen volume growth for the third month in a row. ‘Ready to cook’ is the fastest growing category, with volume up by 36.8% on the year and 45.1% in the last 12 weeks to 27th December.

Total UK beef and veal production in 2020 increased by 2% compared with 2019 to 931,000 tonnes, the highest since 2011. Prime cattle slaughterings rose 2%, mainly due to an increase in heifer numbers, which were up by 4%. Young bull slaughterings were down by 5% on the year, the fourth consecutive yearly decline.

Lamb

Similar to beef, the lamb trade has also made an impressive start to the year. After breathing a sigh of relief following the trade deal with the EU, lamb producers saw the deadweight SQQ price increase by 50p per kg to average 569p per kg, for the week ending 16th January 2021. This is some 114p per kg above the same week last year, which itself was the highest for the last 5 years. The liveweight price, however did fall back, but is still 42p per kg above the same week at the beginning of 2020. The domestic lamb price has been supported by a reduction in imports, driven in particular by a decline in shipments from New Zealand. Total imports fell by 9% in November compared to 2019. This was the lowest import level for the month of November since 1997. Imports from New Zealand for the month declined by 10%. For the whole year to the end of November, imports were down by 7%. However, exports have also seen a decline, particularly to our main trading partner, France. Demand from France has been hit by the Coronavirus pandemic, with volumes to the country down by 27% in November compared to the same month in 2019. In total November saw a 17% decline in exports, compared to year earlier levels.

Pork

Over-supplies of pork and lower pig prices on the continent continue to pull the domestic price down. According to the AHDB, GB prices are still amongst the highest in Europe, but for the week ending 16th January 2021, the EU-Spec SPP fell by 1.7p per kg to average 143.1p per kg. This measure is now nearly 20p per kg less than last year. Because of lack in demand and Covid-related disruptions at processors, market ready pigs are being kept on farms and carcase weights keep breaking records, now averaging 90.96kg up by 250g on the week. Clean pig slaughter numbers did see a year-on-year rise in December by 5%, but this was not enough to offset the declines in the previous two months and market ready pigs remain on farms.

Dairy Roundup

Muller

Muller has announced a new scheme to incentivise its 600 direct suppliers to improve their environmental impact, herd health and supply chain collaboration. The new Muller Advantage programme will commence in January 2021 and will pay 1ppl annually for the measures which reduce antibiotic use, source sustainable animal feed, reduce energy and water usage, recycle, and enhance biodiversity. The new Programme replaces the Muller Direct Premium (1ppl for improving herd health) which ran for a year. In addition, participants will be able to continue to commit a proportion of their milk against fixed prices and future contracts to reduce their businesses exposure to milk price volatility.

Prices

At the latest Global Dairy Trade (GDT) held on 1st December, the average index rose by 4.3% to $3,261. All products saw a rise, as demand from China increases following a post-Covid recovery in its economy;

WMP +5% to $3,182

SMP +3.6% to $2,889

Butter +3.8% to $3,986

Cheddar +2.4% to $3,734

Anhydrous milk fat +2.6% to $4,278

Butter Milk Powder +13% to $2,731

Lactose +13.5% to $1,004

There have been relatively few farmgate price announcements in the UK for the New Year. This could be because purchasers are waiting on the Brexit outcome. That said, those who have announced changes have been positive. Sainsbury’s Muller and Arla aligned suppliers will receive a 0.27ppl price increase from 1st January and First Milk members and suppliers to Belton Farm will receive a 0.25ppl and 0.5ppl rise respectively from the New Year. Saputo, has announced its price will stand-on until 1st February, furthermore it has announced there will be no price reductions during the first quarter of 2021.

Meat Market Update

Beef

Prime cattle deadweight prices declined in the first week of December but still remain firm. Refer to Key Farm Facts for the GB deadweight price for all finished steers. It shows how prices have risen since the end of May and are about 43p per kg deadweight above the same week last year and also in the region of 24p per kg dw above the five-year average. Prices are currently higher than for the same week in any of the last five years. Tight supplies are helping to support prices and this is expected to continue. The latest data from BCMS (October) shows the numbers of prime cattle available (12-30 months) are 5% (83,400 head) less than last year. Beef females and males are reportedly down by 3% and 4% respectively and dairy males by 19% as more sexed semen is used in the dairy herd.

It is therefore disappointing to see a decline in prices at a time of year when you would expect demand to be increasing. It is perhaps due to uncertainty over Brexit. There are reports that some of the UK supermarkets may be favouring Irish beef in the short-term and leaving GB cattle ‘in reserve’ in case there are interruptions to imports come 1st January.

Lamb

The GB finished lamb price has remained strong throughout the autumn and has been on the rise again since the end of October (see Key Farm Facts). The GB deadweight SQQ is about 50p per kg above last year’s level for the same week and 80p per kg above the five-year average. Weekly prices have been at five-year highs since July. This has had a knock-on effect on store and breeding sheep sale prices which have also been strong, particularly in the light of a possible No Deal Brexit.

But why are finished prices so good? It seems tight domestic supplies and strong lamb prices in France are supporting GB values. According to the AHDB, in November the UK lamb kill was 6% lower than last year (1.16m head) and the lowest since 2015. In June and July lambs were coming to market more quickly than usual, but this has not been maintained. Furthermore, adult sheep slaughter is significantly behind last year, with November 20% less than in 2019. This lower level of adult kill may see more lambs being carried over into the New Year for slaughter as fewer lambs are required for replacements. Or, perhaps, due to strong prices this year, intentions have shifted to keeping more sheep and we may see the breeding flock expanding. The outcome of Brexit is likely to inform this decision.

With 40% of all UK lamb exports going to France, developments there are key to the UK price. At the end of November the French reference price for deadweight heavy lambs was 76p per kg higher than in 2019 and over £1 more than the five-year average. Tight supplies have caused the increase in price – demand has actually fallen in France due to closures in the food service market because of Covid. Are UK producers being lulled into a false sense of security with the high finished, store and breeding values? French imports of UK sheep meat have already fallen this year by 14%. If the UK does not agree a trade deal with the EU, prices in France may rise higher, but the value of sheep meat in the UK would decline as a substantial tariff would apply, making UK exports less competitive.

Pigmeat

The finished pig price has seen a steady decline since July. The EU-spec SPP is now about 10p below year-earlier levels, but still nearly 5p per kg more than the five year average. Coronavirus and ASF in Germany are impacting values. Reports suggest there is a backlog of pigs accumulating on UK farms as abattoir throughputs are being restricted due to Covid-19 measures. The total number of clean pigs slaughtered in November was 6% less year-on-year and 7% lower than October figures. Consequently, according to Defra, clean carcase weights in November were 0.82kg more than in October and 3.59kg heavier than last year; the heaviest average clean carcase weight on record.

In Germany, where China’s ban on German imports is still in place due to ASF in the country, the European market is having to absorb the majority of this product. Consequently this is putting downward pressure on EU prices, which has extended to the GB market.

Live Animal Export Consultation

The English and Welsh Governments have issued a consultation on banning the export of live animals for slaughter and fattening. The Governments are also consulting on wider proposals to improve animal welfare in transport. These include reduced maximum journey times, increased space requirements, stricter rules on transport in extreme temperatures and tighter rules for transporting live animals by sea. The consultation can be found at; https://consult.defra.gov.uk/transforming-farm-animal-health-and-welfare-team/improvements-to-animal-welfare-in-transport/ It closes on the 28th January.