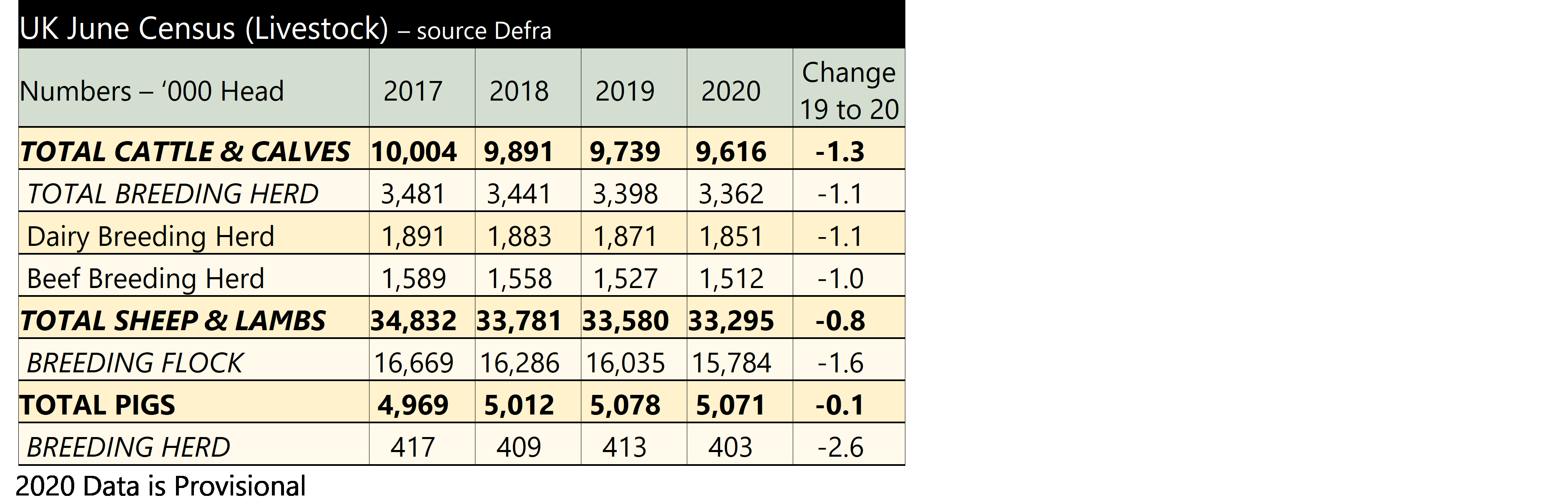

The results of the provisional June 2020 Survey, recently published by Defra, show all the main categories of UK livestock have declined in number over the past year underlining the uncertainties facing the sector. The table below summarises the figures.

The total number of cattle and calves has continued to fall and is at its lowest level since the basis of data collection changed in 2009. Both the dairy and beef breeding herds continue their historic decline. The finished beef price has improved this year, but has been been very poor in the recent past. In dairy, some parts of the sector were hit hard when the food-service sector was locked down due to Coronavirus, with many introducing a harsh culling policy to reduce production. Looking at the Survey results it is only in the category of animals aged less than one year where there is any year-on-year increase in numbers, meaning breeding herds are likely to continue their decline for the immediate future.

The sheep breeding flock has also recorded a year-on-year drop, with all categories showing a fall in numbers. This may be due to uncertainty ahead of Brexit. However, autumn sales of breeding sheep and store lambs have been strong, which would indicate otherwise. It should be noted that the June figures tend not to be the best guide to future breeding intentions as the Survey occurs before autumn cullings and the sales; strong finished lamb prices may have changed intentions held earlier in the year. The December Survey figures provide a better indication of the coming lamb crop.

Total pig numbers have decreased slightly from 2019, although they are still higher than any other year since 2004. But the breeding herd has declined by a relatively large amount; on the back of good margins this is rather puzzling. However, gilts intended for first time breeding have recorded a 3.5% year-on-year increase so we should see some herd rebuilding. The fact that total pig numbers is only marginally down though, implies production per pig is increasing. The full Survey results can be found at https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/925327/structure-jun2020prov-UK-09oct20.pdf

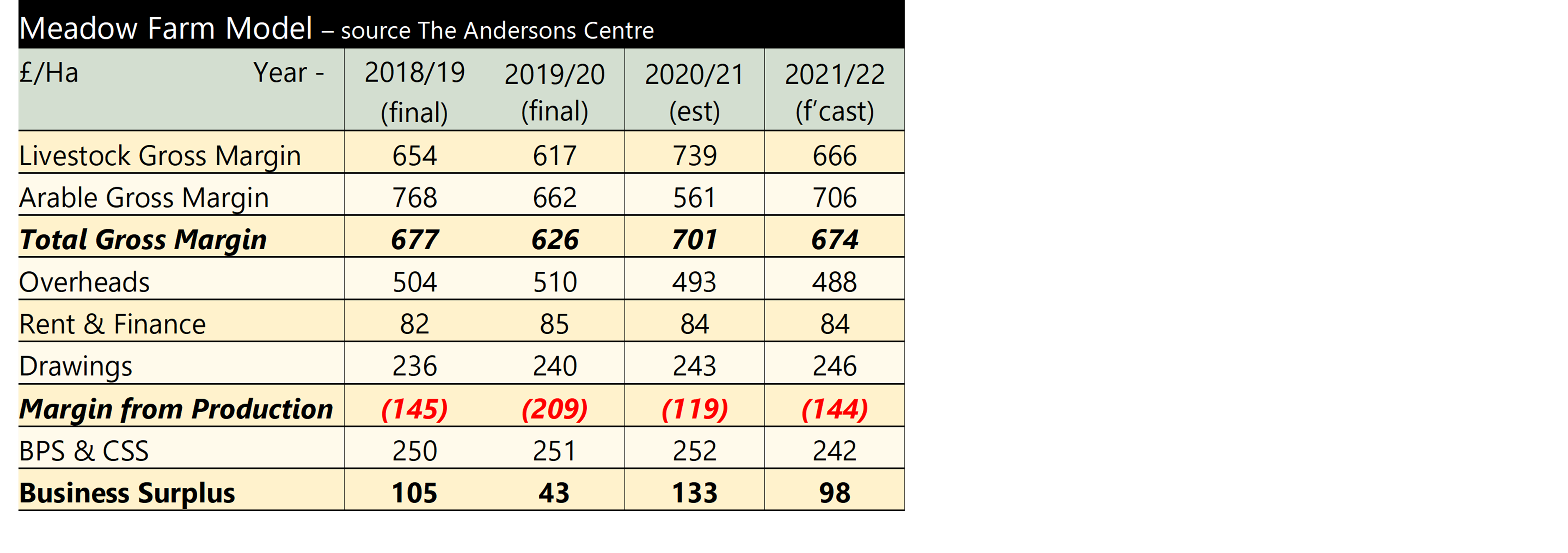

Looking ahead to 2021/22, notwithstanding the possibility of a No Deal Brexit, the sheep price is forecast to decline. But if we do not get a Trade Deal with the EU, Meadow farm could experience a much sharper fall in sheep prices. The beef price is also expected to drop back from its current high as more cattle become available. In contrast, the crops gross margin is forecast to increase as yields recover to a more ‘normal’ level next year. Overheads continue to fall, as a lack of confidence in the industry over Coronavirus and in particular Brexit, sees the proprietors of Meadow Farm refraining from investing. The margin from production remains negative, similar to 2018/19 and it, again, takes the BPS and CSS to provide any profit. This is lower though as the BPS is reduced by 5% in the first year of the BPS Transition, which will see direct payments reduced to zero by 2028.

Looking ahead to 2021/22, notwithstanding the possibility of a No Deal Brexit, the sheep price is forecast to decline. But if we do not get a Trade Deal with the EU, Meadow farm could experience a much sharper fall in sheep prices. The beef price is also expected to drop back from its current high as more cattle become available. In contrast, the crops gross margin is forecast to increase as yields recover to a more ‘normal’ level next year. Overheads continue to fall, as a lack of confidence in the industry over Coronavirus and in particular Brexit, sees the proprietors of Meadow Farm refraining from investing. The margin from production remains negative, similar to 2018/19 and it, again, takes the BPS and CSS to provide any profit. This is lower though as the BPS is reduced by 5% in the first year of the BPS Transition, which will see direct payments reduced to zero by 2028.