The Agricultural and Horticultural Development Board (AHDB) has released its latest Agri Market Outlooks. According to the Levy Board this has been ‘the most challenging’ forecasting period yet. It acknowledges that, even allowing for the impacts of the weather variations, forecasting production has been easier than demand. Aside from the on-going trade negotiations with the EU and the US, the impact of the Coronavirus on how and where we shop and eat makes predictions even harder than usual. The AHDB has used three scenarios to forecast future consumption depending on how well we come out of the Covid-19 lock-down;

Scenario A – called the ‘Bounceback’, is the most optimistic and is similar to how how we are currently experiencing the easing of lock-down. It has the least impact on the economy; overall GDP for 2020 falls by 8% and the Job Retention Scheme helps to keep unemployment at less than 5%.

Scenario C – is the most pessimistic and assumes that the relaxations to lock-down are short-lived and Covid-19 has a long lasting, deep impact on the economy. It sees GDP for 2020 dropping by 30% and unemployment rising to 21%.

Scenario B – sits in the middle and sees GDP for 2020 falling by 15% and unemployment driven up by 14%.

Beef

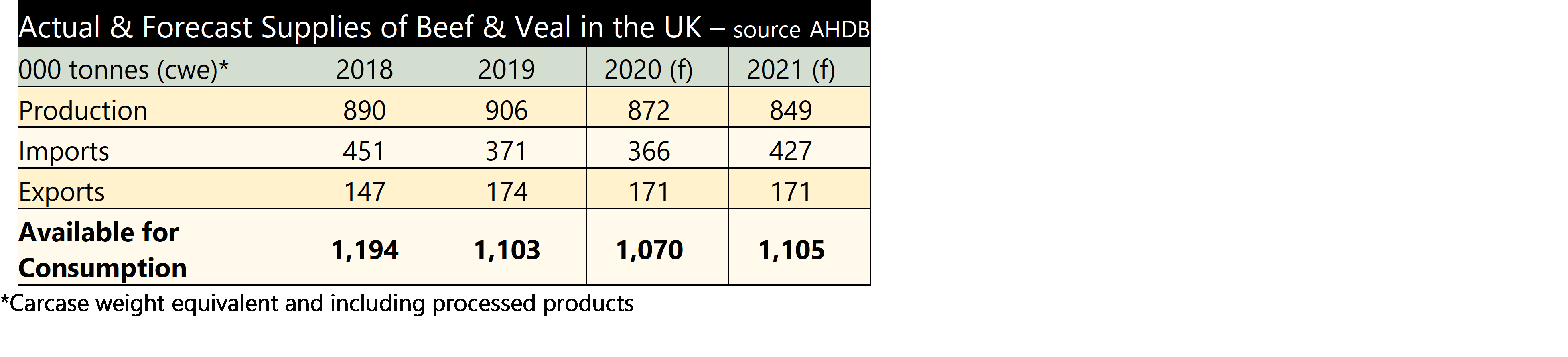

In the beef sector, production is forecast to reduce by 4%. Both the suckler and dairy breeding herds have continued to decline in 2020 and this is expected to carry-on for the remainder of the year. Fewer prime cattle are forecast to be available for slaughter together with lighter carcase weights, all leading to a reduction in production compared to 2019. With regard to trade, both exports and imports are forecast to decline, exports due to a drop in production, but not by as much as previously expected, due to a fall in domestic demand because of Covid-19. The table below summarises the AHDB’s supply and demand forecasts.

In the short-term, the AHDB is expecting beef prices, after seeing a period of recovery, to come under downward pressure due to an increase in Irish supplies and a decline in domestic demand, mainly due to continued weakness in the eating-out market. However, retail sales of beef saw a 22% volume rise, in the 12 weeks to 17th May 2020, according to Kantar, the biggest volume percentage increase out of all the meats, as consumers turned to beef during lock-down. Sales were mainly minced beef, but also good BBQ weather boosted the sale of beef burgers. Supermarket promotions have also helped increase steak sales. But a high proportion of beef has traditionally gone into the food service sector – the highest of all the AHDB’s meat sectors according to volume. During March to May this declined to less than a quarter of its 2019 levels. The temporary closure of the big burger brands saw a significant reduction in the takeaway market.

In the short-term, the AHDB is expecting beef prices, after seeing a period of recovery, to come under downward pressure due to an increase in Irish supplies and a decline in domestic demand, mainly due to continued weakness in the eating-out market. However, retail sales of beef saw a 22% volume rise, in the 12 weeks to 17th May 2020, according to Kantar, the biggest volume percentage increase out of all the meats, as consumers turned to beef during lock-down. Sales were mainly minced beef, but also good BBQ weather boosted the sale of beef burgers. Supermarket promotions have also helped increase steak sales. But a high proportion of beef has traditionally gone into the food service sector – the highest of all the AHDB’s meat sectors according to volume. During March to May this declined to less than a quarter of its 2019 levels. The temporary closure of the big burger brands saw a significant reduction in the takeaway market.

Looking ahead, under Scenario A, beef consumption is expected to reduce by -4% in 2020. Although retail volumes will remain steady for the rest of the year, the losses experienced in the food service sector will see an overall decline in consumption. Any re-imposition of lockdown restrictions would result in a larger drop in consumption as the recovery in the food service sector is chocked-off. Added to that, we could see cash strapped consumers, switch to cheaper alternatives if incomes are hit or unemployment increases, as is the case under the AHDB’s Scenarios B & C, which see beef volumes decline by -8% and -10% respectively.

Lamb

The lamb market is overshadowed by uncertainty from both Covid-19 and Brexit. Due to the large volume of lamb exported to the EU, trade negotiations will have more of an impact on the lamb market than the other meats. Tight UK supplies were initially expected to support prices through the year, but the effects of Coronavirus on the global economy is expected to see both domestic and demand from Europe reduced. The AHDB is forecasting UK sheep meat production to decline by 287,000 tonnes carcase weight equivalent (cwe). In the second half of the year, a lower adult kill more than offsets the marginal increase in prime lamb slaughter and overall production is forecast to decrease by 2%.

Both imports and exports are forecast to decline. Reduced production in New Zealand and high demand in China for protein (due to African Swine Fever (ASF)), means there is less availability for imports. Exports usually follow production trends and therefore are expected to decline, also, due to Covid-19 pressures, demand across Europe could be a lot lower.

Lamb consumption in the UK has been on a downward trend for many years. Even prior to Covid, both in the retail and eating-out market, the volumes for the year were about -4% down compared to 2019. But lamb has been particularly hard hit by lock-down. Whereas overall retail volumes of food and drink grew by 14.7% in the 12 weeks to 17th May 2020, Kantar found retail volumes of lamb actually declined by -7.5%. The lack of gatherings for Easter and Eid al-Fitr did not help, but also the older generation are more likely to cook with lamb and many of these were isolating more.

Looking to the second half of 2020, the AHDB is not expecting the retail market for lamb to grow under any of its Scenarios. Lamb is seen as a less versatile protein and is also more expensive so if consumer household budgets are cut, the switch to cheaper meats is expected. The eating-out market is expected to remain constrained, although lamb has faired quite well in the take-away market, especially kebabs and this will help, unless financial pressures causes a decline in this market. In the best case Scenario, consumption volumes are forecast to decline by -9% worsening to -14% and -19% under Scenarios B and C respectively.

Pig Meat

The AHDB is forecasting UK pig meat production to increase again this year. However due to Covid-19, domestic demand is forecast to decline. Trade is expected to balance the market, with lower imports and increased exports, underpinned by strong demand from China.

The pig breeding herd looks to have increased by 3% last year and challenges to herd performance are easing, production is therefore forecast to increase by 4% in 2020. This is expected to continue into 2021. Imports of pig meat this year were low before lockdown and are not expected to increase due to lack of demand. Imports are forecast to decline by 5% on the year. In contrast, exports are expected to grow by 6% due to increased domestic production and an increasing demand for pig meat from China during the second half of 2020 as the country recovers from Covid-19 and replaces some of its loss of production due to ASF. Next year Chinese production is likely to recover a little and could put pressure on prices.

Out of beef, lamb and pig meat, the latter is expected to have fared the best during the Covid pandemic and as we come out of lockdown, due to its versatility and affordability. For the 12 weeks ending 17th May 2020, pig meat retail volume grew by +14.3% according to Kantar. For the remainder of the year, retail pig meat is expected to continue to do well, all though eating-out losses will result in an overall decline in volumes. As pig meat has a lower price point it is expected to perform better than the other meats if the economic situation worsens. Overall pig meat consumption is expected to reduce by -2%, -3% and -5% under the AHDB’s three Scenarios.

All the July Outlooks can be found at https://ahdb.org.uk/agri-market-outlook?_cldee=cmtpbmdAdGhlYW5kZXJzb25zY2VudHJlLmNvLnVr&recipientid=contact-19608f16c3f347b4b823670087b50991-a2ad3f4987b5401b8357aa27a79c815b&esid=d20000a4-6bbc-ea11-a812-0022480078c7