The AHDB has updated its forecasts for beef production in 2024 and 2025 following an increase in prime cattle and cow slaughterings. According to Defra the number of prime cattle slaughtered in the UK over the first 10 months of the year has increased by 5% compared with 2023, to 1.78 million. The majority of the increase has been driven by heifer slaughter, with the biggest uplift experienced in the 3rd quarter of the year. In October prime cattle slaughter increased 13% year-on-year. This could mean keepers taking advantage of the high prices resulting in fewer heifers being retained for the breeding herd. The year-to-date slaughter numbers in England and Wales have risen by 5%, Scotland has remained stable but Northern Ireland has seen a 12% rise in numbers.

Due to the increase in recent slaughter numbers, the AHDB has revised its slaughter forecast for 2024 upwards to 2.11 million head; 4% higher than in 2023. However, taking this higher slaughter number into account for this year and current UK cattle data, it is expecting a sharper decline in slaughter numbers in 2025. It is now forecasting a 6% reduction compared with 2024 and 2% lower than 2023; totalling 1.99 million head.

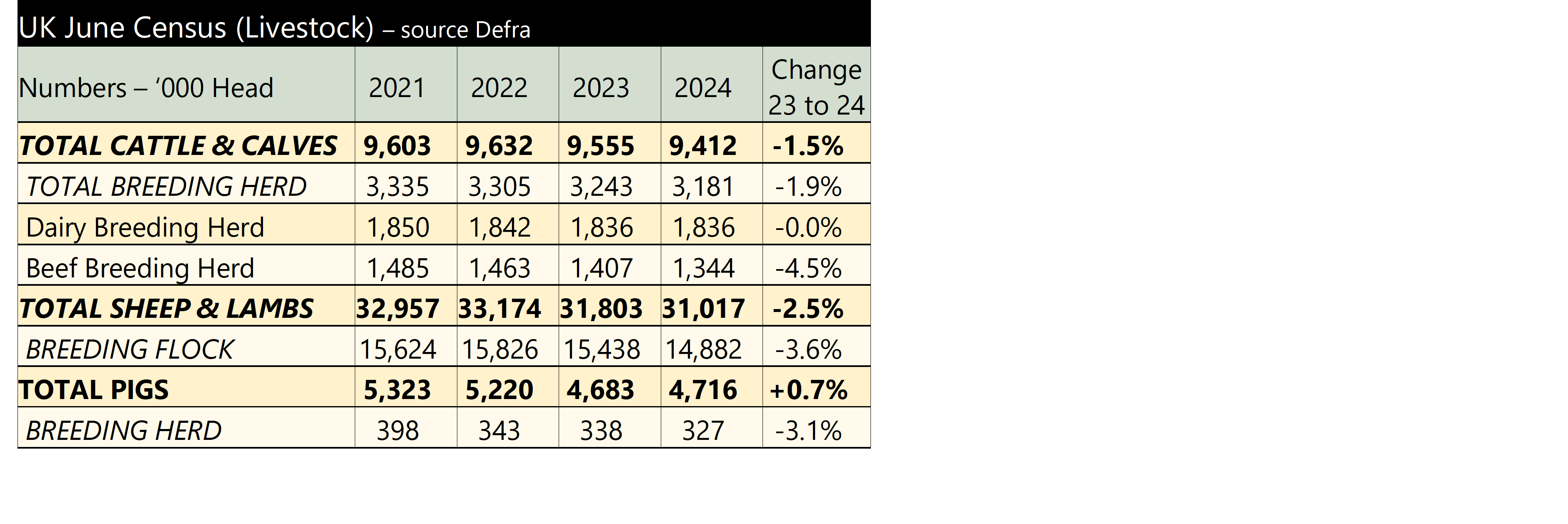

It is a similar story with cow slaughterings. Defra figures show that over the first 10 months of the year, 511,000 cows have been slaughtered, up 3% over the same period in 2023, with the uplift mainly due to beef cows – which is likely to mean further declines in the beef breeding herd, especially as we have already seen an increase in heifer slaughter. Cull cow slaughterings in October were 9% up year-on-year. Again, Northern Ireland has seen a big uplift, a record kill of 47,000, up 13,000 since the previous month. The increase in cow cullings has seen the AHDB revise its figures for 2024 upwards to 624,000 head, 2% higher than in 2023. For 2025 the forecast is for UK cow slaughter to total 599,000, 4% lower than 2024 and 2% less than in 2023.

In terms of beef production, prime cattle carcase weights are averaging 1.4kg heavier than in 2023 at 344kg, this, combined with slaughter estimates, means AHDB is forecasting total UK beef production in 2024 to be 933,000 tonnes – up 4% compared with 2023. For 2025, it is forecasting total UK beef production to decline by 5% on the year and to be 2% less than in 2023 at 883,000 tonnes.

Currently prime cattle prices are at a record high. The GB deadweight all steer price for the week ending 30th November was 538ppkg, up nearly 56ppkg on the year. With supplies being higher than expected, strong demand is supporting farmgate prices. There is usually an uplift in prices as we head towards Christmas, but this good demand should bode well for farmgate prices into 2025.

The economic climate for pig producers, is much better than this time last year, even so the breeding herd continues to contract. The female breeding herd decreased by 3.1% to 327,000. This is the lowest it has been in the past 22 years. However gilts in pig have risen for the second year running, this year by 4.6% (last year by 13%), suggesting some herd re-building is now happening. The number of fattening pigs increased by 0.9%, with falling sow numbers this suggests productivity per pig is increasing.

The economic climate for pig producers, is much better than this time last year, even so the breeding herd continues to contract. The female breeding herd decreased by 3.1% to 327,000. This is the lowest it has been in the past 22 years. However gilts in pig have risen for the second year running, this year by 4.6% (last year by 13%), suggesting some herd re-building is now happening. The number of fattening pigs increased by 0.9%, with falling sow numbers this suggests productivity per pig is increasing.