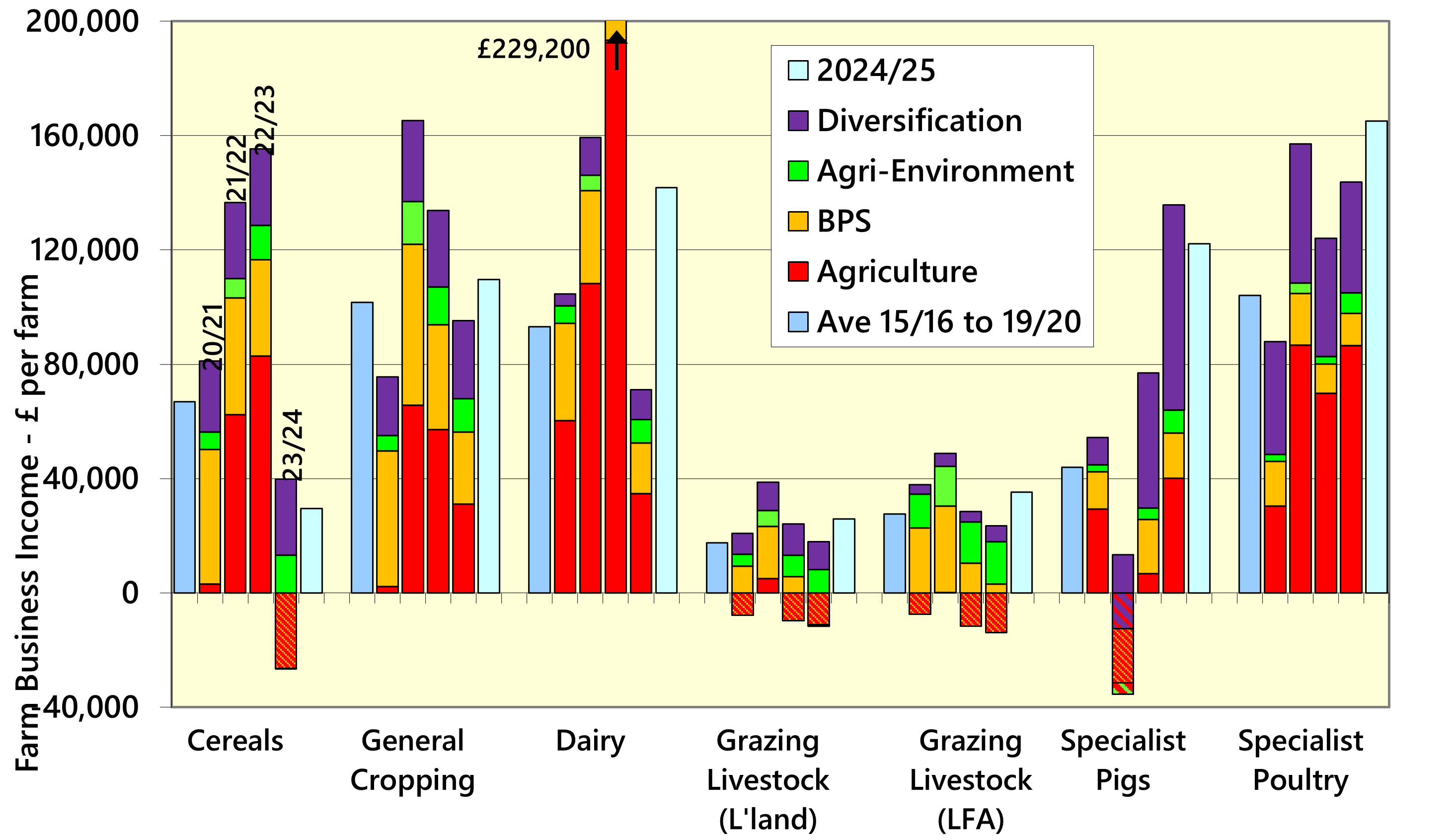

The Finance Secretary, Shona Robinson, delivered the Scottish Budget for 2025/26 on the 4th December. Much like its UK counterpart, this saw farm support maintained in nominal terms, which equates to a real-terms cut once inflation is considered.

The block grant from the UK to Scotland for revenue items actually increases by 1% in real terms for 2025/26. The capital allocation goes up by 7% in real terms. It can therefore be seen that other areas of spending have been prioritised ahead of agriculture.

General policy announcements that will have relevance to farming include;

- the Income Tax thresholds for the two lowest bands will be increased. The Starter band will rise from £2,306 p.a. to £2,827. The Basic band from £13,991 to £14,921. There are no changes to the bands for the Higher, Advanced and Top rates and also no changes to any of the tax rates. The tweaking of the lowest bands has enable the Scottish Government to state that over half of taxpayers will pay less in Income Tax than if they were elsewhere in the UK

- the level of Business Rates will be frozen for 2025/26

- increased funding will go into the Rural Tourism Infrastructure Fund (RTIF) with the aim of boosting visitor numbers and their spending.

Focusing on farm funding, the Budget announcement stated ‘£660 million for support’ – this actually appears to be £657.3m in revenue payments. This compares with £663m estimated for the current 2024/25 year and the actual of £626.2m for 2023/24. Thus, around the same budget in nominal terms, with no uplift for inflation. The budget lines for BPS, Greening, Coupled payments and LFASS are all the same for 2025/26 as in 2024/25. Spending on Agri-environment is forecast to drop from £25m to £21.5m next year.

The £657.3m will be topped-up by £23m of capital spending under an ‘Agricultural Transformation programme’. This is part of the £43m previously taken from the agricultural budget. The remaining £20m is due to be returned in 2026/27. It is not currently clear how the Agricultural Transformation progamme will operate or what it will fund.

There is also funding in the wider Scottish Budget for forestry, advice, animal health & veterinary, land reform, the Islands, marine, natural resources, and research & analysis. The full breakdown of spending for Rural Affairs, Land Reform and the Islands can be found at – https://www.gov.scot/publications/scottish-budget-2025-2026/pages/11/ .