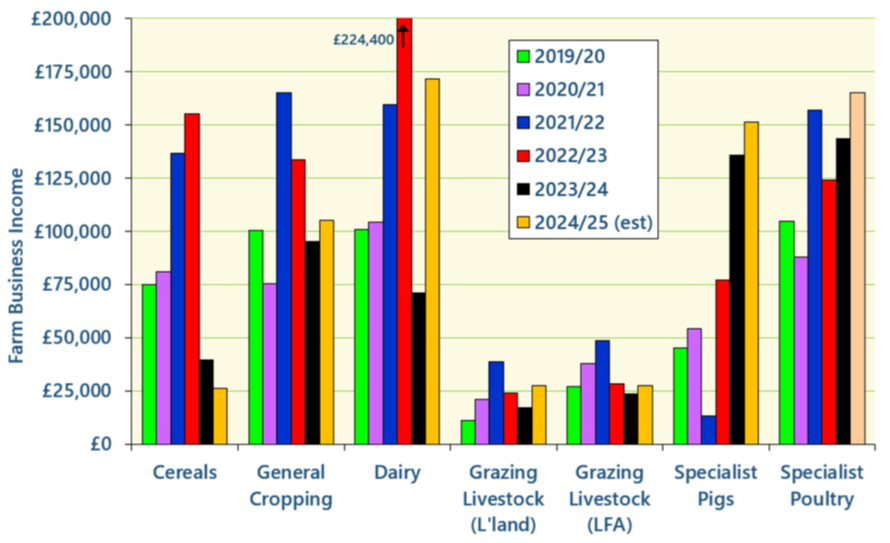

Profits rose for all farm types in England in 2024/25, apart from Cereals Farms. This is according to the forecasts of Farm Business Income (FBI) recently released by Defra. These results come from Defra’s first estimates for FBI for the period March 2024 to February 2025. These include the 2024 harvest and 2024 BPS. They are preliminary estimates at present, with more detailed figures due to be published in November. Although titled ‘income’, what the data shows is average net profit for a typical farm in each sector. The chart below summarises the data for the past few years – all figures are in real terms at 2023/24 prices.

FBI on Cereal Farms is forecast to drop again this year, due to a combination of challenging weather conditions and lower output prices. The output from crops, most notably wheat, is expected to record a substantial decline for the year and, although costs fall, the FBI is forecast to drop by nearly a third to £27,000. For General Cropping farms, lower output from cereals is forecast to be partially offset by increases for other crops, such as sugar beet and potatoes. This, along with lower inputs costs, is expected to result in a 13% rise in FBI to £108,000.

A recovery in the farmgate milk price means FBI on Dairy Farms is forecast to increase by 140% (in real terms) on the year to £176,000. For the Grazing Livestock sector, stronger farmgate prices, particularly for sheep and a reduction in feed costs is estimated to increase FBI for both LFA and Lowland Farms to £28,000. However, for Lowland Farms the main driver is expected to be a substantial uplift in agri-environment income; this is forecast to more than double from the 2023/24 level to around £23,000 in 2024/25. For Specialist Pig Farms, lower costs, particularly feed, are forecast to be one of the main drivers increasing FBI by around 11% (in real terms) to £155,000.

Defra has not made an estimate for FBI in the Poultry sector, so the figure shown on the chart is our forecast.

For the 25/26 year just starting, it currently looks like being another ‘up horn, down corn’ year. Prices in the arable sector are lacklustre, although yields are not expected to be as bad as last year. Lower grain prices should help the livestock sector due to reduced feed costs, together with strong farmgate prices. However, it can be seen from the chart above, that the Grazing Livestock sector is starting from a very low base. It has historically been reliant on the BPS and the fact that the main driver for a rise in FBI is due to a substantial increase in the agri-environment income shows how reliant this sector is now on the SFI and how difficult it will be for those who have not managed to get into the scheme .

Details can be found at –https://www.gov.uk/government/statistics/farm-business-income/forecasts-of-farm-business-income-by-farm-type-england-202425 Actual survey results for this period will be published in November 2025.