Everything grain marketing is focused on new crop by this time of the year, even the remains of the old crop respond to new crop market fundamentals. So prices are moving based on the reports of crop development and of rain or sun. Hence, the markets at this time of year fluctuate far more than the well-being of the developing crop in the ground. This volatility is of less importance in the spring as farmer selling tends to slow, as has been the case this year too. Sales are even slower than normal, as a result of farmers trying to assess what they might have to sell. Inevitably, for many this will be less come September than usual.

The US Department of Agriculture (USDA) in its May bulletin released figures showing ample wheat stocks, sending wheat prices down. But the growing conditions around the world are not great at the moment. The Russian new crop is suffering more than the UK from dry conditions and the crop expectation there has been reduced several times by the local analysts. Across the EU, similarly, crop prospects are being trimmed back by dry soils from the UK across the Northern European belt. At the time of writing. the outlook remains warm and dry. With the UK wheat crop almost inevitably less than 10 million tonnes, and possibly considerably less, the London wheat futures have been gradually rising. This has also been supported by a weaker currency.

Maize demand is starting to rise again with the resumption of an ethanol market in USA. The same is happening for oilseed rape in the European markets with biodiesel demand restarting again. This, coupled with the anticipation of oil guzzling restaurants reopening soon in the UK and Europe has led to higher oilseed rape prices. Coupled with a very low OSR stock level in Europe gave the market a £10 per tonne boost.

The same factor has been positive for malting barley; hints that physically distanced bars might be able to reopen soon have supported the malting sector. Furthermore, the dry soil conditions have pushed down the yield expectations for the large area of spring barley, trimming the potential total crop size. Again, this holds true for Europe going right across the Black Sea regions. Rain is needed badly in the whole of Europe.

The pulse market has reached its high point, having risen to levels that don’t calculate to export to buying destinations. Trading is still quiet as Ramadan continues, but is in its last week. There might be some new crop business thereafter, but probably only when prices come down slightly.

The release of the UK Government’s import tariff schedule this month explains the charges exporters will have to pay to send grain to the UK after the departure of the UK from the EU-Brexit Transition Period on 1 January 2021. The tariffs to import wheat and barley from third countries will be £79 per tonne and £77 per tonne respectively. We normally export these crops but this year this may not be the case due to the low crop size. Therefore these tariffs might have a market effect. However, the import tariff for maize will be zero, suggesting maize can flood in from France and the Americas easily. Thus maize is likely to be the feed-grain import of choice. Furthermore, the high specification wheat will also not have a high tariff, suggesting the milling wheat demand will be sufficiently met.

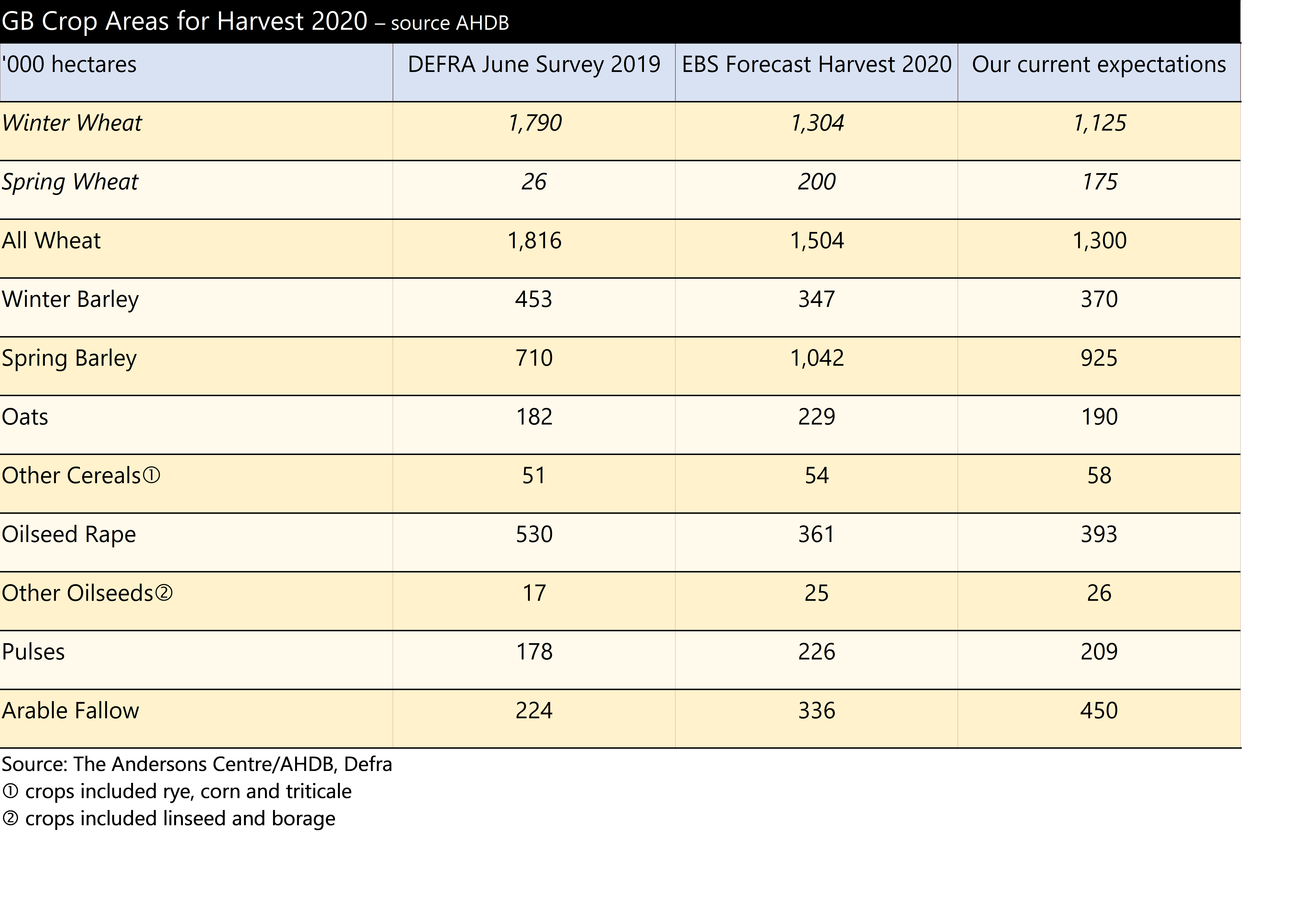

If this projection is correct, it would leave potentially the lowest wheat area planted in the UK since 1978/79, and the highest spring barley area since 1987/88. Some projections expect spring barley to exceed 1 million hectares but we are not convinced there is enough time for that to occur. Oilseed rape area might end up being the lowest since 1988/89. Even so, it still might be the highest we see again because the difficulties of growing the crop this year have been only partly because of the rain, and partly because of the flea beetle. The fallow land area we have suggested here would be the highest level since set aside was mandatory back in 2007. For 2020 autumn drilling and the 2021 harvest, we would expect a high proportion of farmers very keen to capitalise on the first wheat opportunity, possibly planting a little earlier than this year too. Hold tight for a big wheat crop next year.

If this projection is correct, it would leave potentially the lowest wheat area planted in the UK since 1978/79, and the highest spring barley area since 1987/88. Some projections expect spring barley to exceed 1 million hectares but we are not convinced there is enough time for that to occur. Oilseed rape area might end up being the lowest since 1988/89. Even so, it still might be the highest we see again because the difficulties of growing the crop this year have been only partly because of the rain, and partly because of the flea beetle. The fallow land area we have suggested here would be the highest level since set aside was mandatory back in 2007. For 2020 autumn drilling and the 2021 harvest, we would expect a high proportion of farmers very keen to capitalise on the first wheat opportunity, possibly planting a little earlier than this year too. Hold tight for a big wheat crop next year.