The combinable crop harvest is all but finished; the combine harvester has returned to its shelter where it spends over 90% of its time. The few days of work it does is critical but inevitably hugely expensive. It is a shame there is not a cheaper way to get crops threshed and off the field.

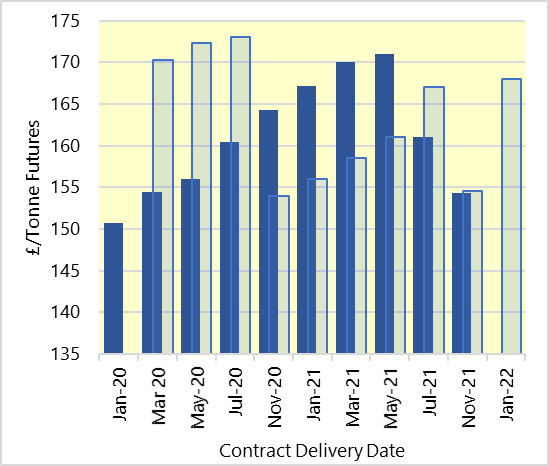

Wheat prices for 2020 harvest have shot up in August and September, from a recent low of £161 per tonne to today’s high of £182 per tonne (November 2020 Futures position). Publications from the US Department of Agriculture have been showing an increasing global wheat crop size, bearish for wheat prices, but a larger decrease in maize production. This is the underlying fundamental affecting the base of all grain prices. Despite the recent reduction in forecasts, output is still 50 million tonnes higher than last year, so the market will not be struggling to source grain, suggesting that unless the local shortage is the main driver, the price spike could be short lived.

This sort of price has not been seen for feed wheat for a couple of years when it reached £193 per tonne for November on the Futures. Consider however, that it was only above today’s level for a month and the same could happen again. Once the feed compounders start switching to feed barley which is trading at a phenomenal £40 per tonne discount, then it will generate a cap in the market. As far as the calorific content of the grain is concerned, barley calculates at about 9 to 10% less than wheat, meaning its proportional value to wheat at £180 should be about £160 per tonne.

The large discount for barley probably exceeds most predictions, but the wheat-barley spread was always likely to have grown this season, with the large barley crop harvested and small wheat crop. We have also seen a poor quality barley harvest. Whilst there will be enough malting barley for making malt for the beleaguered brewers, most of the surplus cannot be shipped as malting, so instead finds its way into the considerable feed barley pile. Scotland is the odd one out and had a good harvest with ample high quality, low nitrogen malting barley, suitable for the malting sector and for shipping down to England.

Is there more barley than wheat? Well, no, but the demand for wheat is higher than for barley (pigs and poultry eat mostly wheat), the demand for feed barley is limited (sheep and cattle do not eat so much grains) and our export outlets also better developed. The UK will be importing considerably more wheat than it exports this season, and that will cause interesting logistical issues as our ports are not so well adapted at importing than exporting grains.

Overall oats appear to have harvested in reasonable condition. Pulses on the contrary have a high percentage of insect damage.

The last fortnight of dry conditions has facilitated a neat end to what began as a tricky harvest period. It is currently raining hard outside my window, which is now a comforting sight for many who were thinking a drop of rain will start the drilled seeds growing.