The UK had a record-breaking cereals harvest in 2019. No records have been broken this year, perhaps apart from the percentage of oilseed rape written off or the percentage decline in wheat crop from one year to the next!

According to provisional Defra estimates, the total wheat and barley crop was over 18.5 million tonnes – nearly 6 million lower than last year, and all of that decline was because of less wheat (the fall in winter barley was more than compensated for by the rise in spring barley).

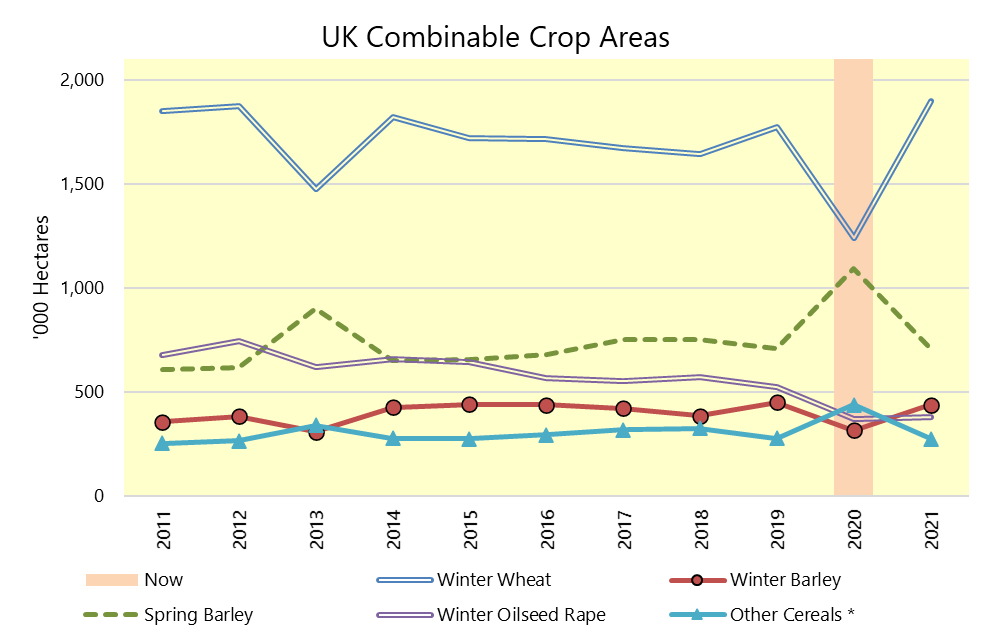

The chart shows the main combinable crop areas for the UK for a decade. Under ‘normal’ conditions, crop areas vary slightly from one year to another according to shifting market requirements and other economic influences as well as perhaps a small weather effect. About once every 7 or 8 years, we see greater shifts in cropping because of inclement weather covering large proportions of the country. That is not to say we can predict when the next weather event will be of course.

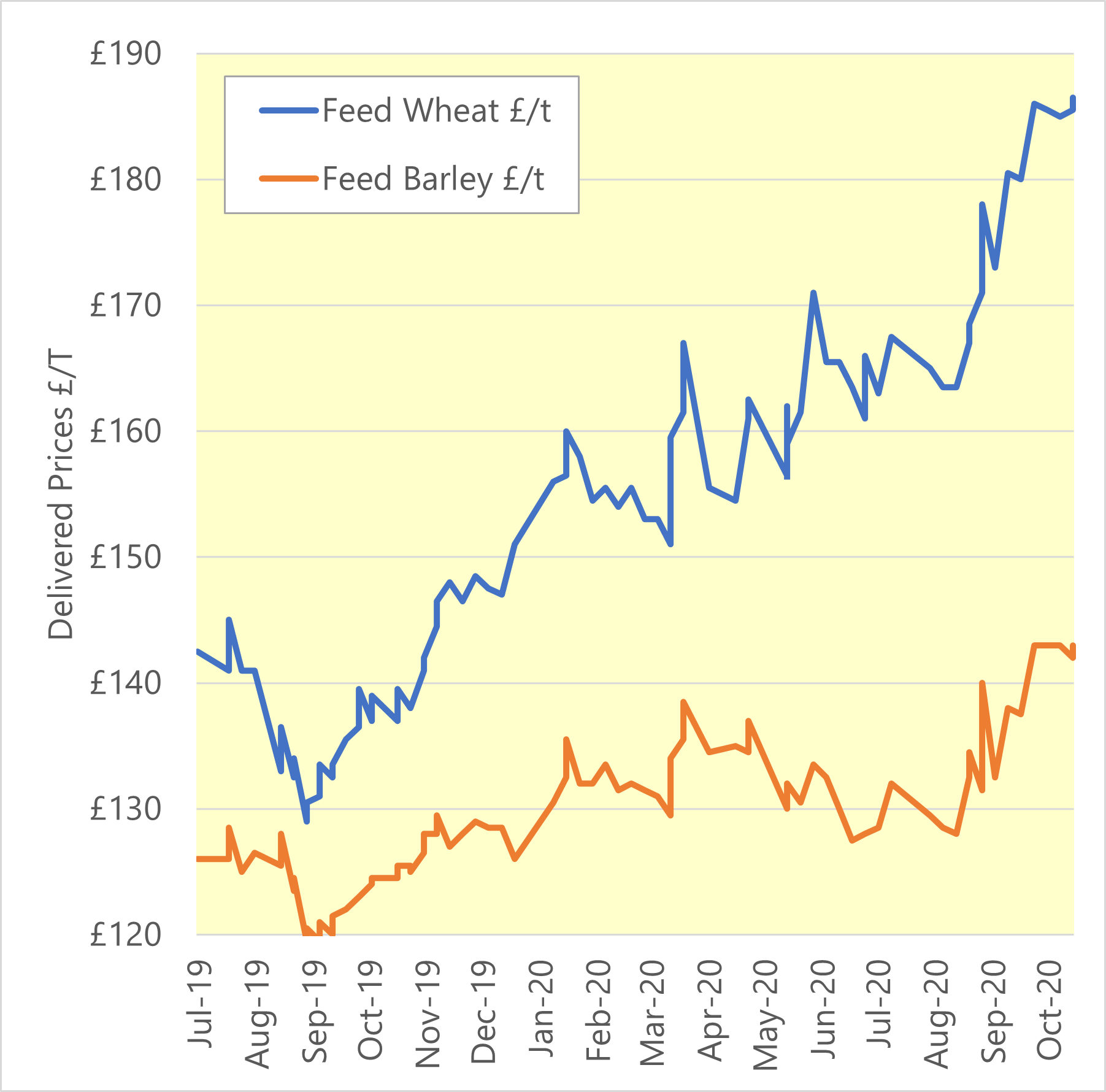

The change in the crop rotation was clearly dramatic, and the amount of resultant crops for marketing is equally unusual. Whilst farms have a different make-up of the crops they want to sell, the market demands are much the same. There is a mis-match, which will drive imports and exports to balance supply and demand and is also causing sharp price movements. Prices for wheat have spiked in recent weeks, having risen by over £20 per tonne for since harvest. The unusual market also explains why barley has not followed suit as it often does, instead, a price spread over £40 has emerged as evidenced in the graph below.

Demand for malting barley is slim, as Covid restrictions close pubs and bars throughout the country and beyond, reducing their already severely reduced requirement for beer. The considerable pile of spring barley is finding ample buyers but for feed. Prices have picked up a little but continue to trade at considerable discounts to wheat in many parts of the world. The new crop price spread is smaller but still £15 to £20 per tonne. The figure below shows delivered feed wheat and barley prices in UK and illustrates the growing spread between the two crops.

The oilseed rape market for anybody who has any to sell, is thin and, as usual, is led not by OSR, but the soy and palm oil markets. The lack of OSR in this country has very little impact on prices. Global vegetable oils are highly susceptible to currency markets and political moves, particularly regarding the relationship between the US and China. Brexit has little impact on the oilseeds markets as they have no tariffs. Brexit negotiations affect these markets more because the strength of Sterling changes according to trade deal news.

The pulse trade is small at the moment having become slightly overpriced to other protein markets. Overall bean quality is not great this year, lowering the overall crop value.